Snowflake (SNOW +1.54%) is the creator of the Data Cloud, a platform where large organizations can aggregate their valuable information even if it’s stored across multiple cloud providers like Amazon Web Services and Microsoft Azure. This is critical for performing comprehensive analysis and extracting actionable insights.

Unified data sets are also vital for developing artificial intelligence (AI) models because real-time access to the most up-to-date information improves their ability to produce accurate outputs. Snowflake built a platform called Cortex AI where businesses can develop and deploy AI, and it includes a growing suite of software products to help collect data, plug it into third-party models, and bring finished apps into production.

Snowflake stock is down 20% so far in 2026 as investors generally are trimming their exposure to the software space. But the overwhelming majority of the analysts tracked by The Wall Street Journal have given the stock a buy rating, and none recommend selling. Their consensus price target points to significant upside from here, so should investors buy the dip?

Image source: Getty Images.

Positioned for the AI revolution

The Cortex AI platform includes a number of AI-powered software features. Document AI, for example, allows businesses to quickly pull data from unstructured sources like contracts and invoices, which used to be a time-consuming manual process. Then there is Cortex Search, which enables employees to immediately locate critical data from across the organization using natural language.

Cortex also hosts numerous ready-made large language models from leading third parties like OpenAI, Anthropic, and Meta Platforms. Businesses can plug their data into these models to create custom AI software applications, which is a faster and cheaper alternative to building entire models from scratch.

Snowflake had 13,328 customers as of Jan. 31 (the end of its fiscal 2026 fourth quarter), and 9,100 of them were using at least one of its AI features. That was up from just 4,000 customers using its AI products a year prior, so uptake is happening fast.

Decelerating revenue growth and growing losses

Snowflake generated $4.5 billion in product revenue during its fiscal 2026, which was a 29.1% increase from the previous year. That growth rate was marginally slower than in fiscal 2025, when product revenue expanded by 29.8%. While this doesn’t sound like a major negative at face value, slowing growth is concerning in the context of the company’s ballooning costs.

Snowflake’s operating expenses jumped by 18% to a record $4.6 billion during fiscal 2026, led by increases in marketing spending and research and development spending. This resulted in a record net loss of $1.3 billion.

Today’s Change

(1.54%) $2.55

Current Price

$168.34

Key Data Points

Market Cap

$58B

Day’s Range

$164.12 – $169.71

52wk Range

$120.10 – $280.67

Volume

187K

Avg Vol

6M

Gross Margin

66.30%

The bottom line looked better after one-off and noncash expenses were excluded: Snowflake delivered an adjusted net profit of $465.9 million for the year. However, those noncash expenses included a whopping $1.7 billion worth of stock-based compensation distributed to employees. That expense shouldn’t be dismissed by investors, because every time the company issues new shares, it dilutes existing shareholders.

When a company is spending a record amount of money, investors want to see that its outlays are paying off. If Snowflake’s revenue growth were accelerating, some of its troubles on the bottom line would be easier to overlook. But I’m concerned there is a lack of organic growth, meaning that when the company trims costs like marketing to narrow its losses, its revenue growth could lose significant momentum.

Wall Street is bullish, but Snowflake stock isn’t cheap

The Wall Street Journal tracks 52 analysts who cover Snowflake stock, and 40 of them have given it a buy rating. Five others are in the overweight (bullish) camp, while the remaining seven recommend holding. None recommends selling.

They have an average price target of $248.07 on the stock, which suggests that it could climb by 43% over the next 12 months or so. However, the Street-high target of $500 implies a potential upside of 189%.

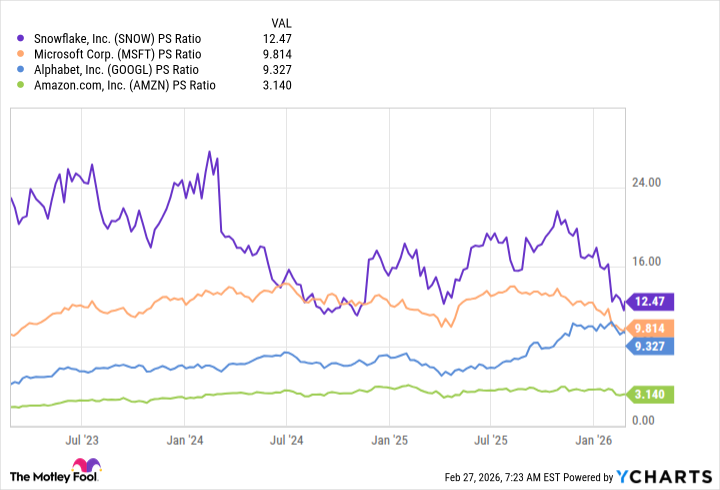

I’m not sure those price targets are realistic. Snowflake is trading at a price-to-sales (P/S) ratio of 13.2 as I write this, and while that is near a three-year low, I would argue the stock is still pricey. This company doesn’t have many comparables in the public markets, but it’s far more expensive than the major cloud providers now offering similar portfolios of AI products and services.

SNOW PS Ratio data by YCharts.

Amazon, Microsoft, and Alphabet operate several businesses outside of cloud computing and software, so they aren’t the perfect companies to compare with Snowflake. However, it’s worth noting that Microsoft’s cloud division generated revenue growth of 39% during its most recent quarter and that revenue from Alphabet’s Google Cloud rocketed higher by 48% in the same period.

Since Snowflake is growing at a much slower pace, its premium valuation is tough to justify, in my opinion. Investors might want to wait for a deeper correction before they buy this stock, regardless of Wall Street’s bullish consensus at the current level.

{kind=link}