Dell Technologies Inc.’s founder-led business is one of the most remarkable and under-appreciated stories in tech. Dell Technologies is not particularly sexy, nor does it put forth an earth- shattering vision that bends the mind. Yet it’s a company that has consistently figured out how to ride successive waves without becoming driftwood.

And like Hyman Roth of Godfather fame, founder Michael Dell (pictured) always seems to make money for his partners. Unlike Roth, Mr. Dell is not a gangster, rather he’s a gentleman who literally wrote the book on how to play nice and win.

In this Breaking Analysis and ahead of Dell Technologies World 2025 in Las Vegas, we examine the question of how will Dell capture the explosive artificial intelligence opportunity, while transitioning the millions of servers, storage arrays and PCs it already has in the field to this new AI era?

Premise: Winning enterprise AI hinges on three factors

We believe Dell’s ability to stay out in front hinges on three imperatives, including: 1) Doubling down on full-stack “AI factory” systems that collapse infrastructure silos and accelerate time-to-AI value; 2) Unlock the latent power of its massive global channel — treating 200,000-plus partners as an extension of the direct engine rather than a bolt-on; and 3) Modernizing the core — that is, redesigning servers, storage and networking for highly parallel, power-hungry workloads while relentlessly driving down cost per floating-point operation and attacking the energy footprint customers now scrutinize.

Decoding Jeff Clarke’s revenue arc slide

Below we show a chart Chief Operating Officer Jeff Clarke unveiled at Dell’s 2023 Financial Analyst Meeting in October 2023.

The image depicts a time-series line that surges through key milestones in tech. We see in the 1990s the direct-to-consumer PC model takes off, then accelerates again in the early internet era when e-commerce turbocharges that same motion. Around the early 2010s the curve flattens — then dips — illustrating Dell’s struggle to morph into an enterprise powerhouse, jettisoning its relationship with EMC and moving forward on its own with 30-plus acquisitions such as Compellent, EqualLogic, Boomi, Perot Systems and many more, including several software assets. This ultimately proved to be an expensive learning exercise. The line rebounds sharply post-2016 after the EMC deal, peaks with the VMware stake, and now turns upward again as Dell positions itself squarely in the AI wave.

Why it matters

In our view the slide is more than a history lesson; it’s a roadmap. Dell’s strategic pivots — private-equity reset, EMC megamerger and VMware monetization — set the stage for the current AI cycle. The task now is to translate that hard-won enterprise footing into end-to-end AI factories, monetized via a revitalized channel and powered by infrastructure that balances performance with energy pragmatism and an enticing value proposition for enterprise customers, relative to hyperscalers.

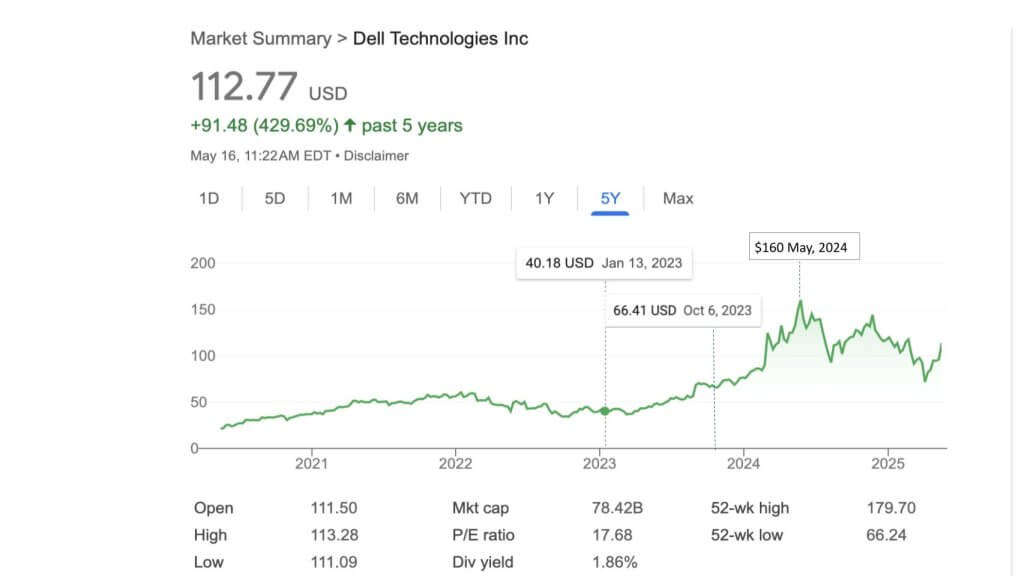

Dell’s valuation: from overlooked to AI-fueled outperformer

Dell’s equity story aligns with the market’s awakening to generative AI. The five-year stock chart shown below highlights January 2023 with the shares at around $40 — valued well under one times sales.

- January 2023 – “ChatGPT awakening.” OpenAI’s holiday buzz turns into the early days of AI hype, with board rooms trying to understand the imperative. Investors at that time began factoring AI optionality into infrastructure names, but Dell is still priced for slow growth.

- October 2023 – Analyst Day inflection. Michael Dell lays out the vision and Jeff Clarke conveys the execution plan for riding the next wave – the thesis we discussed earlier. The stock catches a tailwind as buy-side models reset growth and margin assumptions in a post-VMware world with a much stronger balance sheet; Dell simultaneously pulls new capital allocation levers – buybacks and a steady dividend; the Street loves that story.

- Spring 2024 peak. Shares rip to ~$160, a 4x multiple expansion in roughly 15 months, marking the high-water mark of early AI exuberance.

- Today – rationalization phase. The stock hovers near $112 — still 3x the pre-AI baseline and up ~430% since the pandemic, reflecting more balanced views on supply constraints, gross-margin mix and capital intensity.

Visually, the chart shows a long flat-to-slightly-down channel from 2020 through 2022, a sharp diagonal ascent beginning Q1 ’23, an acceleration post-Analyst Day, and a gentle step-down to the current level — essentially a classic hype-cycle “installed base” plateau.

Capital return as a structural tailwind

AI is only half the story, perhaps even less. Dell returns ~80 % of free cash flow to shareholders, Michael Dell included, through repurchases and dividends. That framework resonates with value-oriented funds that previously ignored the name. The flip side, of course, is that sizable buybacks imply management sees limited return on investment in incremental R&D or M&A. Whether that tradeoff is sustainable as AI factories scale will be a key watch-point in upcoming quarters. Dell’s strategy appears to be focus on keeping costs down, making structural changes internally, applying AI to improve efficiencies and driving EBITDA and cash flow through the roof.

As we said, it’s not sexy, but it’s lucrative.

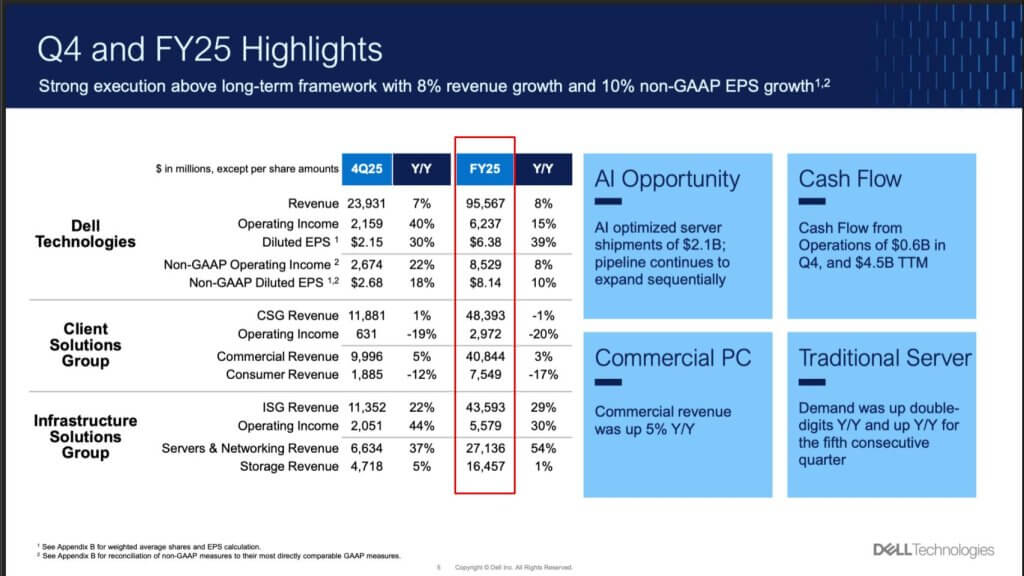

Dell revenue engine: two segments, one supply-chain flywheel

The slide below from Dell’s financial reporting distills the company’s P&L into two main vectors comprising the bulk of its nearly $100 billion in total revenue for fiscal 2025. The business is split almost evenly between its two reporting segments.

- Client Solutions Group (CSG) – Focus on commercial PCs

Roughly 55 % of revenue. A classic low-margin, high-volume business that anchors Dell’s global supply-chain leverage. - Infrastructure Solutions Group (ISG) – enterprise gear

Roughly 45 % of revenue. Inside this business, ISG itself bifurcates:

• ~60 % servers and networking – mid-teens gross margin; Intel Corp. historically captured most silicon economics, a role Nvidia Corp. has now assumed in AI servers.

• ~40 % Storage – 45% to 50% gross margin; still Dell’s profit engine, albeit below the mid-60% peaks EMC once enjoyed.

Why the simple model matters

In our view, the elegance of this structure is strategic. By preserving the PC volume HP jettisoned after its split, Dell keeps purchase-order muscle that wrings pennies out of every component across the stack. That flywheel lowers unit costs for ISG. Moreover, it allows Dell to claim true “end-to-end” status while competitors assemble piecemeal.

Dell’s margin dynamics: the mix shift story

During the early phases of the pandemic, an unprecedented surge in remote-work and at-home learning catalyzed a sharp spike in PC demand. Unit shipments soared, propelling Dell’s top-line revenue to record levels. However, the mix leaned heavily toward lower-margin notebooks. Because these volumes carried thinner product margins and added supply chain costs, the very growth that buoyed revenue simultaneously compressed gross margin, underscoring how a skew toward less profitable products can dilute profitability even in boom times.

Today, the center of gravity has shifted to AI-optimized servers within the Infrastructure Solutions Group. Enterprises and service providers racing to deploy large language model and inference workloads are prioritizing GPU-dense systems with far higher average selling prices and margins. This mix enrichment somewhat offsets Nvidia’s higher silicon vig in each configuration. Consequently, margin expansion is visible despite the absolute dollar outlay for GPUs, illustrating the leverage that premium configurations bring when demand is both urgent and price-insensitive.

Storage mix further accentuates this benefit as Dell controls more of the IP. Looking ahead, we believe the next catalyst will come from a broad-based storage refresh cycle. All-flash arrays shipped in the 2018-2020 window are hitting warranty expiration just as new AI-centric storage architectures – featuring graphics processing unit-direct fabrics, parallel file systems, object stores and greater AI affinity, combined with ultra-low-latency networking embedded into servers — enter mainstream availability.

As customers migrate to these higher-value, high-capacity systems, the shift promises a second-order margin tailwind. In our view, the combination of richer storage average selling prices and recurring software licensing tied to data-services will fortify gross margin even further, extending the profitability uplift that began with today’s AI-server boom.

The software gap

VMware hitting Dell’s P&L once addressed Dell’s software deficiency, but the Broadcom divestiture leaves a hardware-centric portfolio. Management chose liquidity and balance-sheet clarity over folding VMware in and inflating margin optics. The explicit bet Dell is making in our view is that its supply chain scale combined with AI factories will allow the company to compete on value against the likes of Hewlett Packard Enterprise Co. and Amazon Web Services Inc.

In our opinion, Dell’s ~$100 billion hardware flywheel is both its moat and its challenge. Though the company has unmatched procurement leverage on one hand, it faces constant pressure to innovate at wafer-thin PC margins while chasing higher-value enterprise workloads. As much as we would have loved to see a VMware “spin in,” the company appears comfortable with and well-suited to pursue its current model and navigate the challenge.

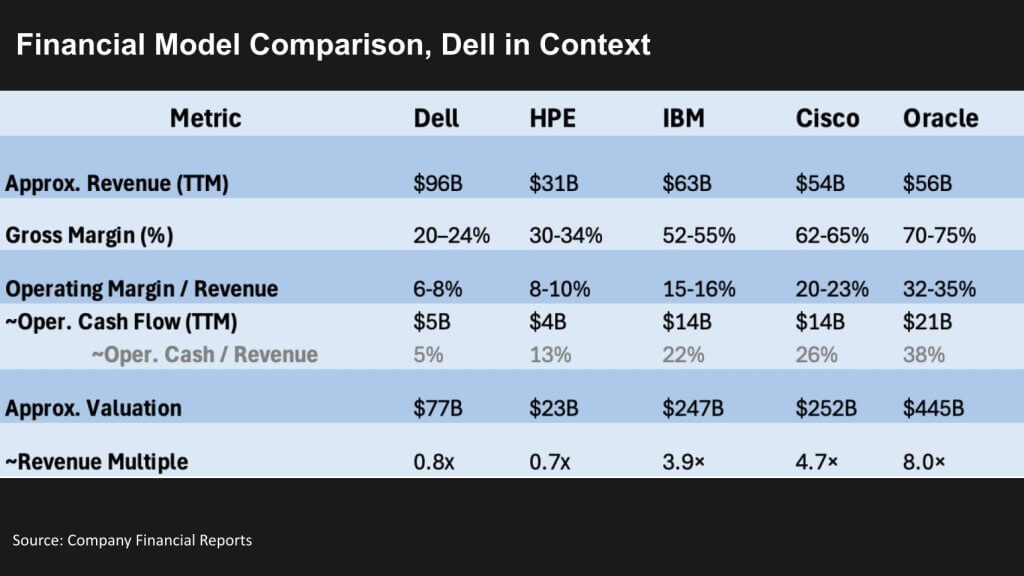

How Dell measures up: the valuation-to-margin continuum

Above we show a comparative table of five tech incumbents — Dell, HPE, IBM Corp., Cisco Systems Inc. and Oracle Corp. — arrayed left-to-right starting with Dell, then ascending by revenue multiple. The rows list trailing-12-month revenue, gross margin, operating margin, operating cash flow dollars, OCF as a percentage of revenue, approximate market cap as of yesterday, and the resulting revenue multiple.

Key messages in the data

- Dell’s supply-chain scale vs. margin reality

Dell’s nearly $100 billion top line dwarfs Oracle’s and Cisco’s, yet its low-20% gross margin pushes the stock to a 0.8x sales multiple—even after a dramatic re-rating. The PC drag remains the structural governor. - HPE: margin relief, but at a cost

Shedding PCs lifted HPE’s gross and operating margins several points, but it lost the Dell-style procurement leverage and cash-flow heft. Investors still accord it only 0.7x revenue. Notably, HPE’s revenue multiple used to be much larger than Dell’s. The combination of AI server momentum and an aggressive return of capital to shareholder policy have flipped that script. - IBM’s software flywheel in action

With software now approaching half of revenue, IBM’s gross margin pushes into the mid-50s, nearly doubling Dell’s operating margin and quadrupling its revenue multiple to 4x. - Cisco: ARR conversion shields the model

Even amid recent routing and security softness, Cisco still monetizes mid-60% gross margins and a high-20s operating margin, supporting a nearly 5x sales valuation. - Oracle’s cloud-plus-software premium

A 70%-plus gross margin and low-30s operating margin drive massive cash generation — more than any peer on the slide — and the market rewards that with an 8x revenue multiple, despite OCI’s capital intensity.

Strategic implication for Dell’s valuation

In our opinion, Dell’s capital-return story and AI server uptick have closed part of the valuation gap, but the table tells a clear story – i.e. hardware scale alone makes it difficult to crack the 1x sales valuation ceiling. To earn a software-style multiple, Dell must: 1) Embed higher-margin intellectual property deeper into its AI factory stack; 2) Find a software engine it can keep this time; or 3) Massively automate with AI, cutting internal costs and driving unprecedented productivity by applying agents to redesign processes.

We believe the third option carries low risk and is well underway. This in and of itself should provide a mid-term valuation boost. It remains unclear whether Dell will tap either or both of the other two options to trade at a higher multiple relative to peers.

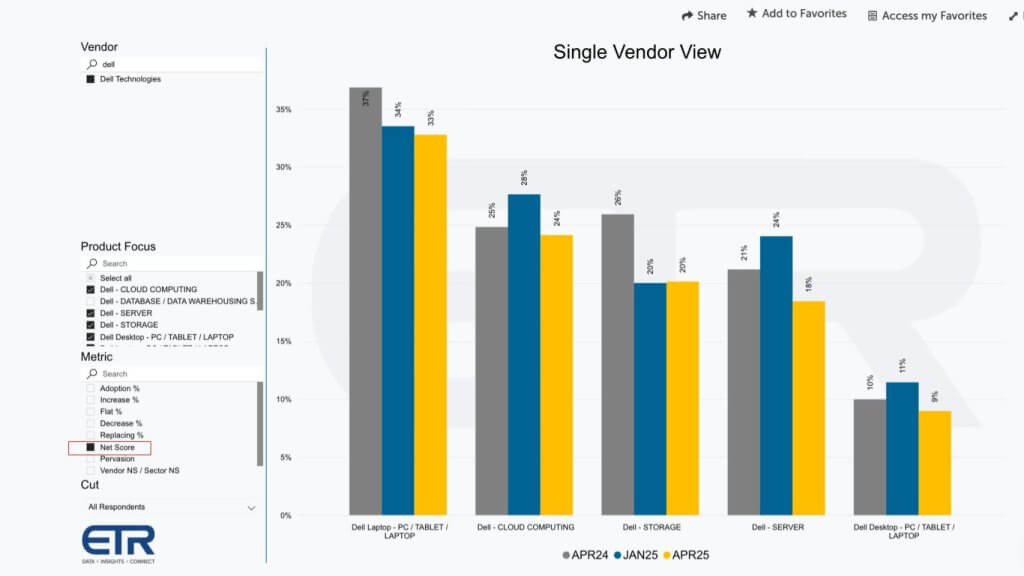

ETR pulse check: Macro headwinds slow spending momentum, Dell still holds pockets of strength

The slide below pulls from Enterprise Technology Research’s quarterly TSIS survey and plots Net Score — the firm’s composite metric for spending velocity — across five Dell categories: Laptops, Cloud Computing (read: private-cloud spend), Storage, Servers and Desktops. Three data points appear for each line — April ’24, January ’25 and April ’25 — letting us track budget sentiment over the past year.

How to read the graphic

- The y-axis is Net Score; anything above 40% is “highly elevated.” Scores in the 20% to 30% range are very respectable.

- Each group of bars represents product segments.

- A red outline frames the Net Score metric we’re focused on, emphasizing that every segment now sits below the 40% breakout zone.

Key observations

- Across-the-board deceleration. Every line drifts south between April ’24 and April ’25, mirroring broader macro budget compression; Dell is not uniquely singled out here.

- Laptops remain the bright spot. Even after softening, commercial laptops post a ~33% Net Score — best-in-class for a mature category and well ahead of servers or desktops.

- Cloud-computing score is “respectable.” It tracks in the mid-20s, solid for a private-cloud–oriented offer competing against hyperscalers’ strong momentum.

- Infrastructure skews lower but stable. Storage and servers hover in the low-20s, consistent with cyclical digestion after the pandemic hardware surge.

Implication

We believe the survey reinforces Dell’s mixed reality. That is to say, macro belt-tightening is tamping down momentum, yet the PC franchise still outperforms and the private-cloud narrative resonates with a smaller but meaningful subset of buyers. The net effect is muted, not collapsing, which sets the stage for an AI-driven refresh cycle to re-accelerate infrastructure spend when and if budgets loosen.

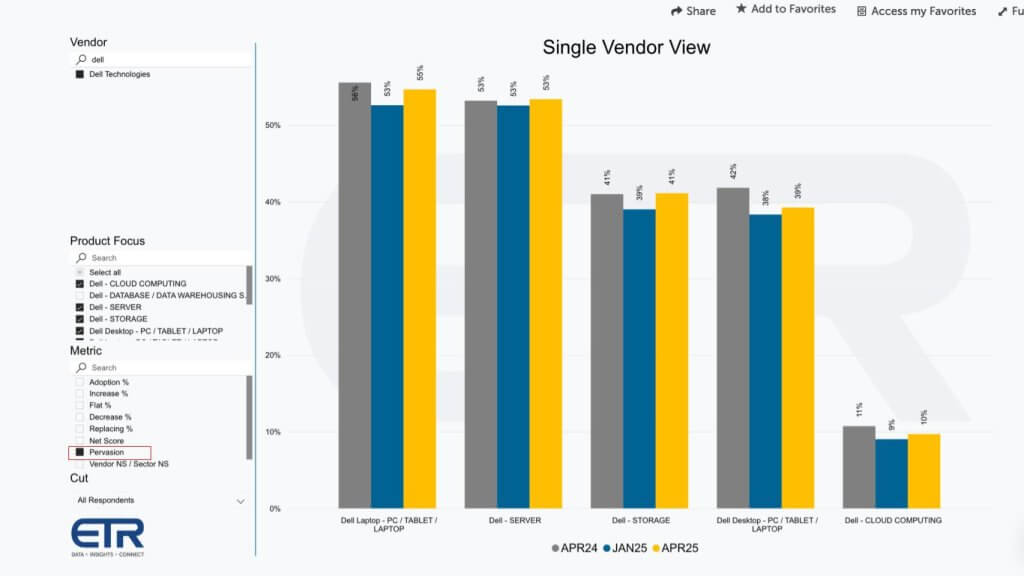

Installed-base gravity: Dell’s Pervasion scores dominate the hardware stack

The slide below takes the same ETR dataset but switches the y-axis from Net Score to Pervasion — the percentage of survey respondents that cite Dell as a current supplier in each category. A red box highlights the metric and the bars immediately show how deeply embedded Dell is across the enterprise landscape, with the exception of cloud.

Visually, the bars for laptops and servers extend above the 50% line, storage and desktops cluster just below 40%, and cloud computing trails in the low teens.

What the numbers tell us

- Laptop and server dominance. More than half the enterprises surveyed run Dell for endpoint and compute — an installed-base moat competitors will find hard to crack.

- Storage still commanding. At ~41% penetration, Dell/EMC remains the leading storage presence even if global share has slipped since the acquisition.

- Desktop hang-on. Nearly 40% pervasion underscores Dell’s continued leverage in traditional PC form factors.

- Cloud footprint modest but strategic. Lower penetration reflects Dell’s focus on on-premises and private-cloud workloads rather than hyperscale infrastructure as a service.

Why it matters

We believe these pervasion stats highlight Dell’s greatest strategic asset – that is, a vast, sticky installed base it can mine for AI-factory upgrades and cross-portfolio pull-through. The challenge — and opportunity — is converting that legacy footprint into next-gen infrastructure before subscription-heavy rivals poach the refresh cycles.

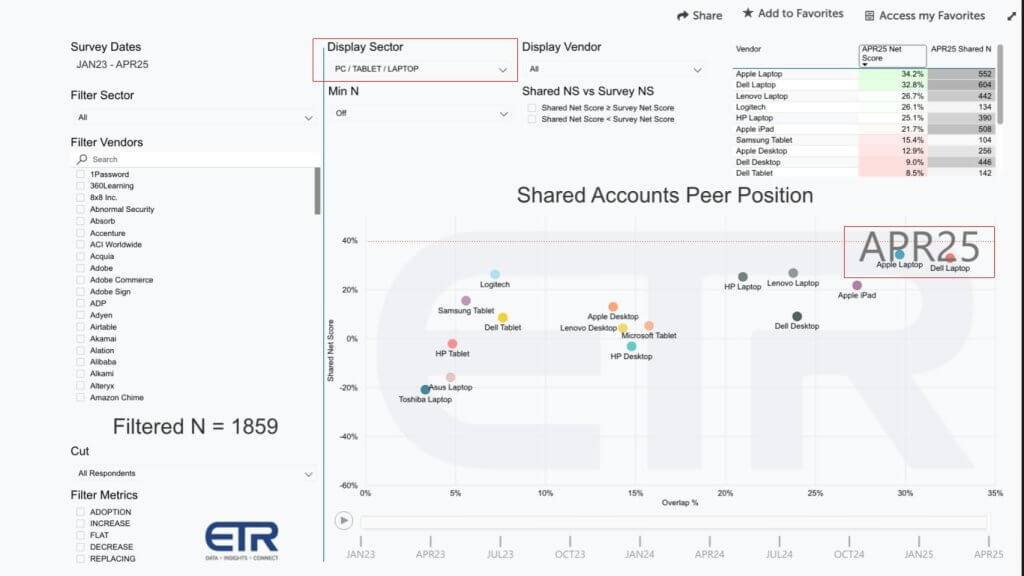

Peer comparison: Momentum meets footprint — Dell laptops square off with Apple

The next slide below is a two-axis scatter plot drawn from the same ETR dataset:

- Y axis (vertical): Shared Net Score — the proxy for spending momentum.

- X axis (horizontal): Penetration (ETR labels it Overlap) — the percentage of the 1,859 enterprises in the survey that actively use each product.

A dashed horizontal line at 40% highlights the “elevated-momentum” threshold; no hardware vendor breaches that bar in this cut, underscoring the budget drag we discussed earlier and the maturity of this market.

What you see

- In the upper-right call-out box we show the category leaders: Apple Laptop at a 34% Net Score and Dell Laptop at 33%. They are virtually neck-and-neck on momentum, with Dell edging Apple on the X-axis thanks to deeper enterprise penetration.

- Every other Dell offering — servers, storage, desktops — clusters lower and left, signaling solid but less explosive momentum against a broader installed base.

Why it matters

Our research indicates that Dell’s commercial laptop line enjoys best-in-class velocity and the broadest footprint, a combination rarely achieved in mature categories. That leadership not only sustains the company’s supply-chain economy of scale but also gives Dell a privileged entry point to upsell edge AI workflows and back-end infrastructure as customers modernize their fleets.

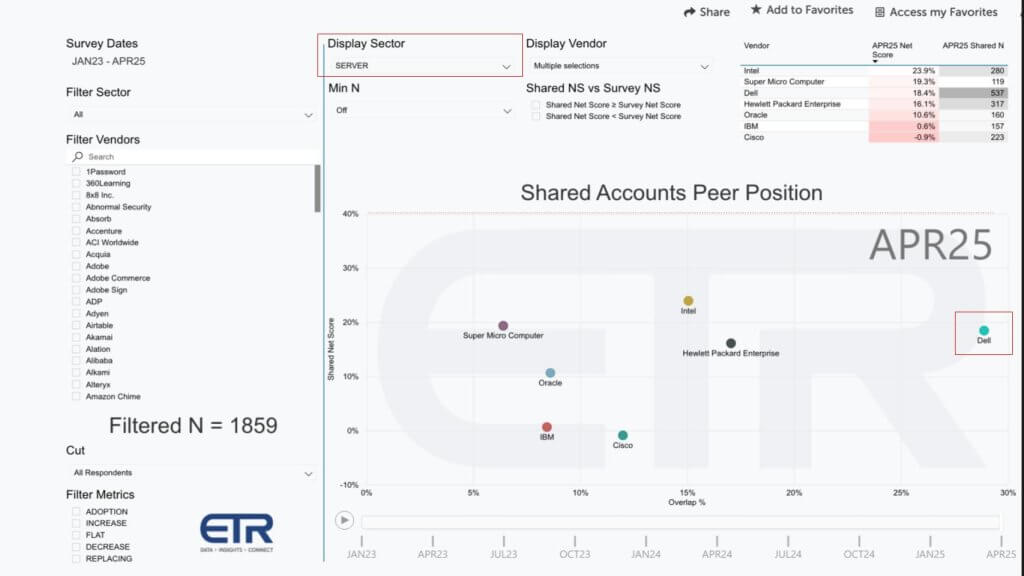

Server landscape: Dell owns the footprint, but momentum signals a mature market

The data below is another ETR scatter plot — Shared Net Score on the vertical axis, Penetration (Overlap) on the horizontal — this time comparing server vendors. The dashed red line at 40% again marks the “high-momentum” threshold.

What the dot plots tell us

- Dell Server sits farthest to the right, based on 537 out 1,859 — meaning 537 of the 1,859 surveyed enterprises run Dell servers. No rival approaches that installed-base gravity.

- Nearby, but a step left, are Intel white-box designs and Supermicro — collectively representing the ODM/DIY crowd. Their Net Scores cluster close to Dell’s, reinforcing that every mainstream server supplier is feeling the same demand profile comprising AI enthusiasm with overall budget compression.

- Importantly, all points reside below the 40% line, underscoring how even AI enthusiasm hasn’t yet lifted server spending into breakout territory in mainstream enterprises.

- In our view this underscores that most of the AI activity today is occurring in the cloud (hyperscalers and neoclouds), while enterprises sort out the skills needed and fill the gaps on today’s somewhat lacking AI stacks.

Implications we draw

- Dominance, not disruption. Dell’s server share remains unequaled; the company controls the refresh clock in more than a quarter of large enterprises surveyed.

- Maturity dampens momentum. With x86 commoditized and hyperscalers soaking up custom silicon, Net Score gains are incremental at best—everyone is fighting for replacement cycles, not greenfields.

- Path to reacceleration. In our view, Dell must pair this formidable footprint with differentiated AI-factory rack designs (accelerator-dense, liquid-cooled, software-tuned), attract startups into its ecosystem and build more robust AI solutions to reignite spending velocity — and, by extension, push its Net Score above current levels.

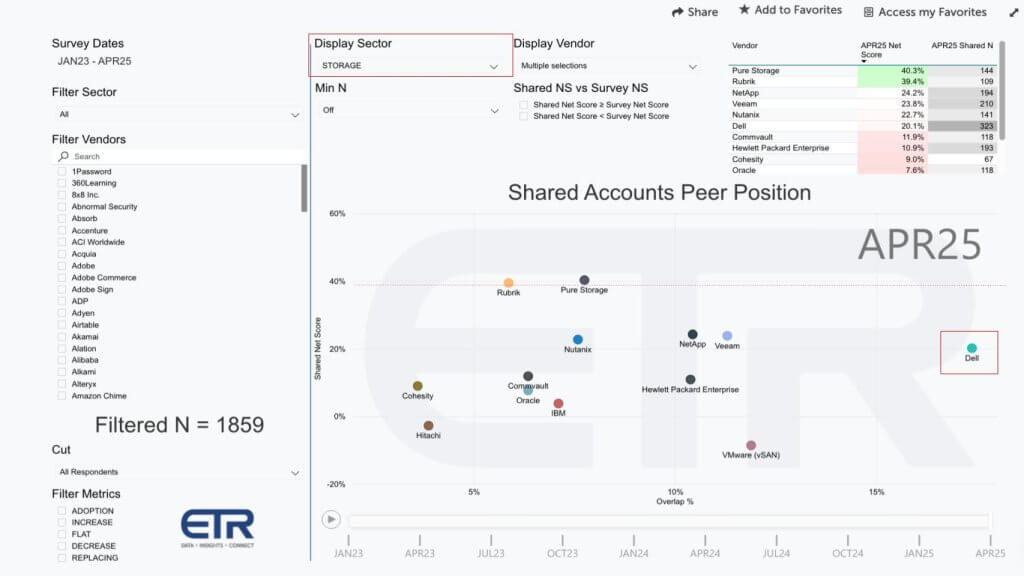

Storage snapshot: Dell’s installed-base moat versus Pure’s momentum

The slide below shows the ETR storage scatter, again plotting Shared Net Score (spending momentum) on the vertical axis and Penetration (Overlap) on the horizontal. Remember, ETR lumps primary storage and data-protection arrays into one category, so the field mixes old-guard storage area network vendors with next-gen and legacy backup platforms.

Reading the plot

- Dell occupies the far-right position, tagged “323/1,859.” Translation: 323 surveyed enterprises — more than any rival — run Dell storage. Its Net Score, however, sits well below the 40% breakout line.

- Pure Storage stands out as the lone dot above that 40% threshold, signaling the highest forward spend in the cohort.

- Rubrik hugs the 40% line, evidence that its rebranding from backup to cyber resilience is resonating.

- NetApp, Nutanix Inc., HPE and VMware vSAN (now folded into Broadcom Inc.) form a middle cluster, showing solid penetration with muted momentum.

Key takeaways

- Installed-base advantage, not momentum leadership. Dell’s 300-plus account footprint underscores decades of dominance, but the spending velocity has shifted to Pure and security-framed newcomers such as Rubrik.

- The AI factory pivot. To keep that base from eroding, our view is Dell must wrap Nvidia GPUs, AI-optimized networking, AI-optimized storage and modern data-protection services into integrated “AI factory” bundles — offering customers a refresh path that marries legacy arrays to accelerator-heavy compute racks. At the same time, offering a wide range of choice across silicon vendors, storage types and price bands.

- Open silicon partnerships remain critical. Though Nvidia is the marquee ally, Dell’s continued alignment with Intel, Advanced Micro Devices Inc., Broadcom and others will prove essential to filling price-performance gaps and preserving margin in an otherwise hardware-heavy portfolio.

In our view, Dell’s strategy is clear: Leverage its unparalleled storage footprint to seed AI-ready infrastructure upgrades, continue to update the portfolio with AI optimized storage (parallel file systems, high performance, disaggregated systems); and then rely on tight partnerships and full-stack integration to reignite the momentum currently captured by more specialized rivals.

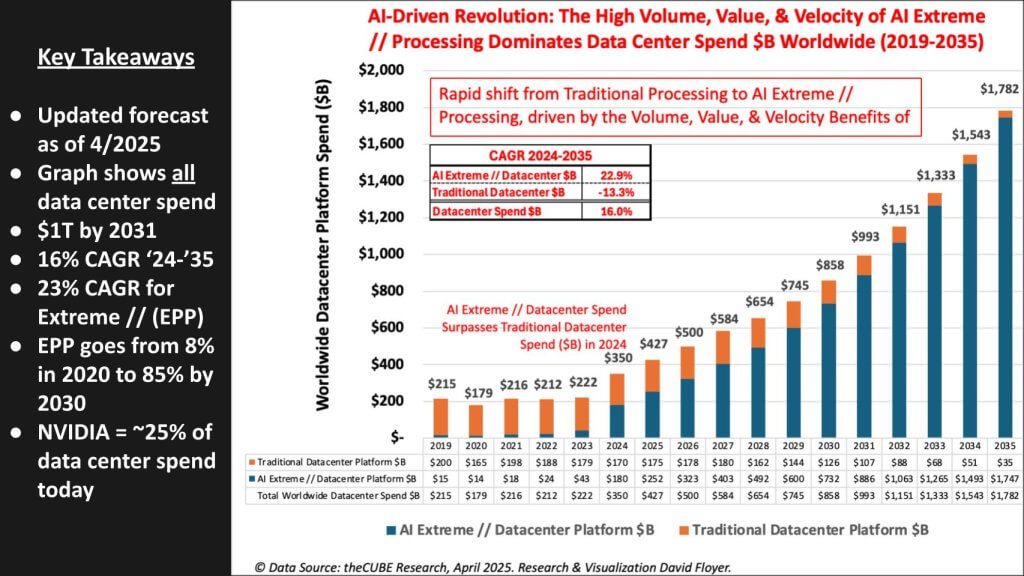

Macro backdrop: a $1T data center overhaul

Our research indicates AI is not merely an incremental workload; it is redefining the entire data-center stack. The graphic below is our April 2025 update to the long-range data-center infrastructure forecast covering facilities, power, cooling, servers, storage and networking.

What the chart shows

- Y axis: annual spending in billions of dollars.

- X axis: calendar years 2024 through 2035.

- Two stacked areas rise year-over-year:

- Orange band — traditional x86 infrastructure. Think classic CPU-centric servers with a sprinkling of IBM Power or mainframe that’s too small to break out. Compressed spend.

- Blue band — accelerated computing/extreme parallel processing or EPP. Purpose-built systems for AI training and inference — GPU, custom ASIC and tightly coupled high-bandwidth fabrics.

A key marker highlights total spend topping $1 trillion in the early 2030s.

Key numbers

- Overall CAGR (’24-’35): mid-teens, squarely in the double-digit “mid-teens” range.

- Accelerated segment CAGR: ~23 %, driving the bulk of total growth.

- Share shift: EPP jumps from 8 % of spend in the COVID era to ~85 % by 2030 — a wholesale flip of the data-center bill of materials.

Why this matters for Dell — and everyone else

In our view, the takeaway is stark – that is, every dollar of traditional x86 spend that flatlines must be replaced, or exceeded, by GPU-dense architectures. Suppliers that master power, cooling and supply-chain economics for AI factories will ride this trillion-dollar wave; those clinging to CPU-only designs risk shrinking into the gray band that barely registers on the forecast by decade’s end. IBM’s Z will survive this transition and x86 will continue to have its place, but the days of dominance for general-purpose architectures are over.

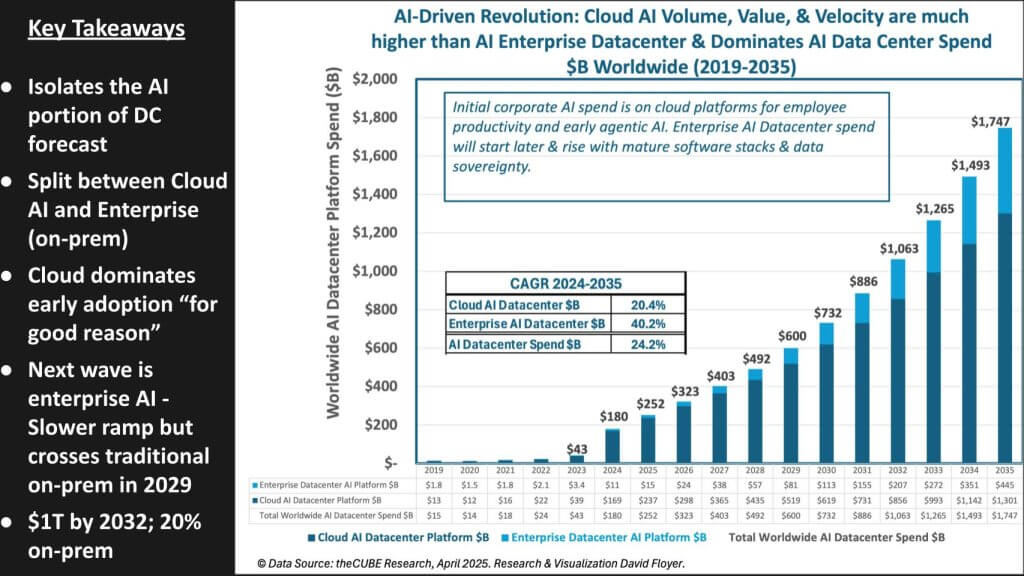

AI spend in focus: Cloud leads, enterprise catches a second-wave tailwind

The chart below strips out non-AI workloads and isolates annual AI infrastructure outlays through 2035. Two stacked areas tell the story:

- Dark-blue band — hyperscale/cloud AI capex. Dominates the left side of the graph, reflecting today’s spend reality. Cloud titans enjoy first-mover advantages. They have the cash, software tooling, and the gravitational pull of existing data lakes so their curve ramps sharply from 2024 and keeps climbing through the decade, though the curve flattens modestly after 2029.

- Light-blue band — enterprise/on-prem AI. Starts as a thin ribbon, then widens steadily, crossing the traditional, non-AI on-prem line from the prior forecast at roughly early next decade and reaching ~20% of all AI data center infrastructure spend by 2032. The area continues to grow into the early 2030s as data-sovereignty and latency requirements force companies to “bring AI to the data.” Note: This assumes that firms like Dell build the ecosystem, solutions and on-prem AI stack required for enterprises to easily adopt.

Note: overall AI infrastructure surpassing the trillion-dollar mark early next decade.

What the Numbers Mean for Dell

We believe Dell is engineering squarely for the AI crossover:

- Installed-base leverage. Hundreds of thousands of x86 servers wearing Dell logos sit next to petabytes of enterprise data that will not migrate to hyperscalers. Modernizing that real estate for GPU clusters, high-throughput storage tiers, and 800-gigabit fabrics is Dell’s home-field advantage.

- Channel reach. A partner network unrivaled in the enterprise lets Dell walk the data-center aisles and land “AI blocks” exactly where workloads reside.

- Twin mandates

- Retool the stack. Ship fully integrated “AI factory” racks — liquid-cooled, accelerator-dense, Ethernet-or NVLink-fabricated — while maintaining open silicon partnerships (Nvidia, Intel, AMD, Broadcom and beyond).

- Harvest and protect the core. Keep the Fortune 500’s traditional workloads going; ensure x86 estates interoperate easily with the new GPU clusters via parallel file systems, vector databases, and policy-based, computational governance.

Bottom line

In our opinion, hyperscalers will continue to set the early pace, but the battleground for the next decade is enterprise AI. Dell’s strategy — “modernize what you have while layering in what you need for AI” — positions the company to capture that second-wave demand when the forecast says on-prem AI spend overtakes legacy infrastructure.

What to watch at Dell Tech World: AI PCs, AI-optimized infrastructure, optionality and lots of model numbers

We expect Dell to emphasize heavy dose of AI PC messaging — hopefully some new adoption metrics, refreshed form factors and a deeper dive on the neural processing unit roadmap. Apple’s early M-series momentum has stoked plenty of chatter around on-device inference; Dell must now prove its AI-chip-plus-NPU strategy can deliver comparable battery life, latency and developer traction.

Full-stack AI factories: Choice is the brand

Expect Dell to bombard attendees with server, storage, and “AI factory” SKUs — an options portfolio that illustrates its core value proposition: customer choice at global scale. We believe the headline themes will be:

- Silicon optionality. Nvidia remains the preferred accelerator, but AMD GPUs, Intel Gaudi and, of course, mainstream x86 all stay on the menu for price-sensitive or inference-heavy workloads.

- Model optionality. Expect shout-outs to Meta’s Llama stack, Hugging Face model gardens and a growing roster of curated “enterprise-ready” smaller language models. Dell doesn’t build a proprietary foundation model; the answer is ecosystem breadth.

- AI-optimized servers, storage and networking. Look for upgrades to legacy PowerStore/PowerScale lines, plus new parallel-file or object tiers tuned for massive checkpoint traffic. On the network side, Dell will bundle Broadcom-based Ethernet fabrics and Nvidia’s InfiniBand to hit the 800-gigabit — and soon 1.6-terabit — marks that GPU clusters demand.

The code-name playbook: from Project X to GA SKU

Dell’s cadence has become predictable: Announce a “Project” one spring, ship the SKU the next. Alpine, Frontier, Fort Knox, Fort Zero, Helix — each followed that pattern. Customers have learned they can scope budgets a year out, but history also shows some projects fade quietly. Caveat emptor: Watch which previous code names and which 2025 “projects” receive firm ship dates versus “tech preview” language.

A more prominent role for Dell Consulting

Dell services has taken on an expanded role in this AI era. Dell recognizes that many customers not only lack an on-prem AI stack but they lack the skills necessary to move fast. Dell Consulting acts as an important accelerant to help customers navigate data quality challenges and governance and privacy concerns; and build solutions that can fit into existing legacy infrastructure while at the same time helping firms lean into the AI opportunity.

Expect services and consulting to be prominently on display at DTW 2025 from laptops to the top of the stack and into managed services.

Execution risks we’re tracking

Our analysis flags four areas that could challenge Dell’s AI ambitions:

- GPU supply still gated. Hyperscalers soak up first allocation; enterprise SKUs arrive later.

- Facility retrofits. Liquid cooling and high-density power draw strain legacy on-prem data centers — particularly the mid-market Dell channel serves.

- Software gap. Cloud platforms bundle developer-friendly sophisticated data stacks, governance and MLOps layers; Dell must lean on partners and solutions to avoid a “hardware-only” stigma.

- Competitive crossfire. Supermicro’s design-to-order racks, HPE’s GreenLake-wrapped AI servers and a crowd of ODMs each court Dell’s own installed base with aggressive pricing and services overlays.

Our take: threading the AI needle

In our view Dell’s differentiation will not come from boasting the fastest GPU node — everyone will hit spec-sheet parity within quarters. The real test is whether Dell can orchestrate an end-to-end AI factory that stitches racks, storage, fabrics, software and services into a turnkey outcome, then deliver it through a channel that already owns the loading-dock badge at most enterprises.

If Dell executes, it can harvest the cash flows of its mature PC and server franchises while expanding wallet share with AI-ready systems for the next decade. The pivot hinges on the following key question: Can those AI factories leap from Tier-2 and Tier-3 service providers into mainstream enterprise halls before cloud vendors lock in the market?

We’ll be on the ground with theCUBE all week to test that thesis—and will report back in Breaking Analysis as the story unfolds.

Photo: News

Disclaimer: All statements made regarding companies or securities are strictly beliefs, points of view and opinions held by News Media, Enterprise Technology Research, other guests on theCUBE and guest writers. Such statements are not recommendations by these individuals to buy, sell or hold any security. The content presented does not constitute investment advice and should not be used as the basis for any investment decision. You and only you are responsible for your investment decisions.

Disclosure: Many of the companies cited in Breaking Analysis are sponsors of theCUBE and/or clients of theCUBE Research. None of these firms or other companies have any editorial control over or advanced viewing of what’s published in Breaking Analysis.

Your vote of support is important to us and it helps us keep the content FREE.

One click below supports our mission to provide free, deep, and relevant content.

Join our community on YouTube

Join the community that includes more than 15,000 #CubeAlumni experts, including Amazon.com CEO Andy Jassy, Dell Technologies founder and CEO Michael Dell, Intel CEO Pat Gelsinger, and many more luminaries and experts.

THANK YOU

{kind=link}