Table of Links

Abstract and 1. Introduction

2. What is Ponzi?

3. The FTX Collapse

4. Future Directions

5. Concluding Remarks and References

3 The FTX Collapse

The story of FTX starts with its founder SBF. Though there already existed hundreds of CEXes and strong competitors such as Coinbase or Binance, SBF still decided to launch a new crypto exchange FTX in April 2019. The growth of FTX was sped up by cooperating with a good market maker Alameda to provide liquidity. Interestingly, Alameda is also founded by SBF. The great collaboration between FTX and Alameda made FTX rapidly grow up to the global Top3 CEX, and made the valuation of FTX balloon in size to $32 billion as of January 2022 [24]. With such success, FTX naturally launched its self-issued token FTT just like most centralised exchanges. However, with all the familiar stages in order – token boom and a fad for it, then leverage and diversion, then problem revealed and panic followed close behind, FTX finally fell into its crash. In this section, we decompose this disastrous speculation and demonstrate three facilitators that explain the FTX collapse, namely FTT, leverage, and diversion.

FTT. FTT is the utility token of FTX centralised exchange, mostly used for lowering trading fees on the platform. Like most other cryptocurrencies, FTT is an inherent Ponzi-type token, meaning that it is not backed by any asset. The FTT issuers raise money from the first wave of investors with a near-zero cost, just like the initiating debt in any Ponzi game. FTT may sustain, or may even achieve a rational Ponzi game if it can maintain a relatively stable or increasing market value and be actively traded in a healthy way. But unfortunately, FTT performs weaker than people previously believed. FTT does not entitle users to a part of the platform revenue or represent a share in FTX, nor give control over governance decisions or FTX’s treasury. However, these are not the very causes of its own collapse, the essence of financial distress is loss of confidence. The change in the mindsets of investors from confidence to pessimism is due to the excessive leverage and divert operations conducted by FTX and Alameda.

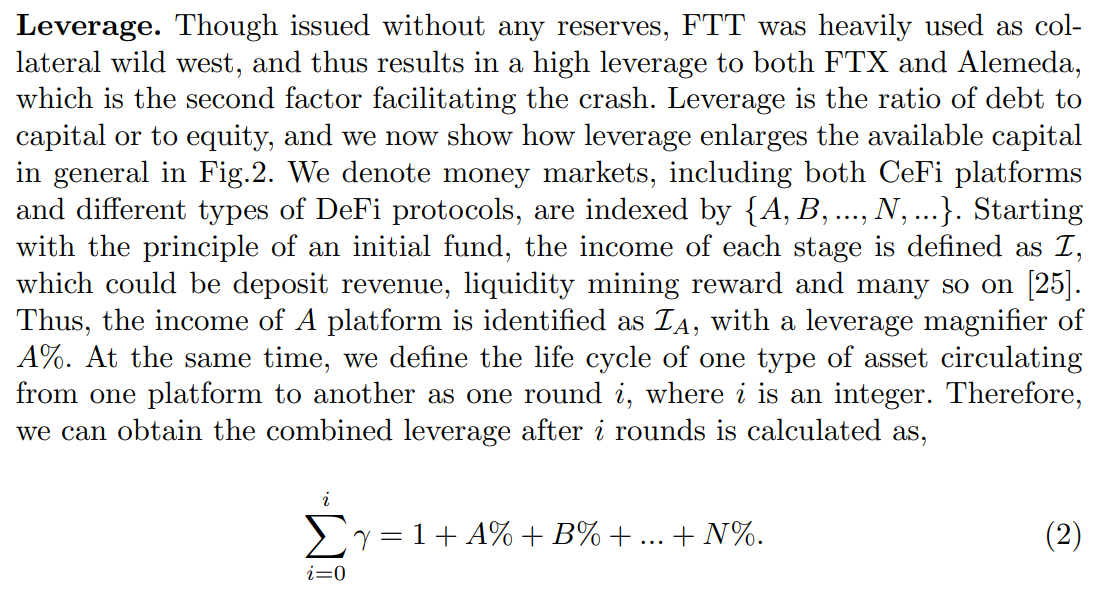

With such financial approach, FTT was used as collateral to raise a significant amount of money in the market, covering a series of CEXes and DeFi protocols, and thus making its virtual value be magnified thousands of times (leverage). At a high level, FTT plays a very similar role of M0 (currency & bank reserves) in traditional finance [26], but the actual impacts of FTT and related derivatives make up M1 (money easily used in transactions), or even M2 (money easily used in or converted into use for transactions and real GDP) [27].

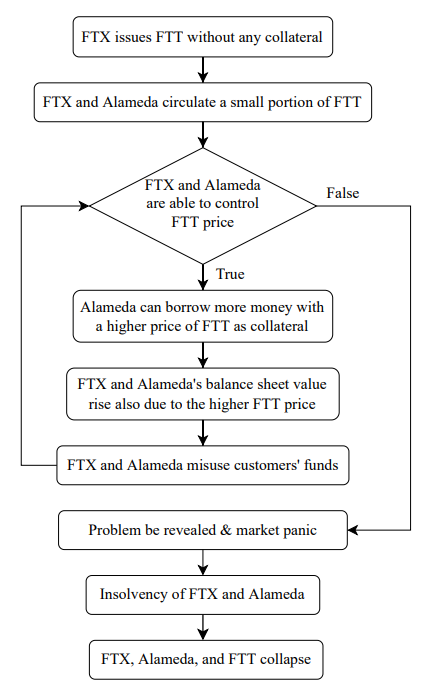

Diversion. In addition to the previous two factors, the misue of customers’ funds also facilitates the FTX collapse all along. As shown in Fig.3, FTX and Alameda only circulate a small portion of the total supply of the FTT, meaning they are able to control the FTT price with funds easily. On top of this, the vast majority of coins were held by FTX, Alameda, and other associated companies. They continuously borrow money from investors and entities with FTT as collateral. To further promote the asset price, FTT managers start to misappropriate the users’ reserves (divert). In this sense, the booming of FTX is vigilant. In retrospect, we know that SBF also spent a lot in donating to political parties, heavy marketing and even bailing out other insolvent companies. But there are nearly no external restrictions on how he can use the funds. The game ends in a panic when all problems are revealed. FTX and Alameda were not solvent, and SBF finally paused the withdrawals, marking the official ending of the story.

The FTX crisis was not isolated but a sequel to the previous Luna/UST failure, also the beginning of a new series of collapses. The previous big collapses of Three Arrows Capital and Terra/Luna meant the market participants were extremely vigilant when it came to any rumors of potential insolvency. The collapse of FTX further damaged the already shaken reputation of the crypto industry. Besides losing customers’ and investors’ funds, the collapse of FTX is already having a knock-on effect on other companies and the overall crypto market. Solana and BlockFi are among the most severely affected projects. We refer readers interested in detailed information on this event to the reports by CoinDesk and Nansen [10] [13]. We may also likely expect to see more affected companies being revealed in the near future, and a slow recovery of belief in this market.

4 Future Directions

With lessons learned from the FTX’s crash, we discuss possible ways for better security and sustainability in this area.

Regulation. Regulation has been debated since the emergence of cryptocurrencies. On the one side, users moving from traditional finance to crypto space are with strong motivations of pursuing decentralization. Regulation is naturally placed in the opposite position. The collapse of FTX raises concerns from users to worry about potential regulatory implications such as heavy regulations or strict policies. However, on the flip side, each time such an influential event happens, a large number of players, unfortunately, run away quickly from crypto. Meanwhile, the leave of some giants makes it easier for the remaining ones to form a monopoly, making regulatory intervention the only viable solution at this moment. Therefore, properly introducing regulation into CEXes and even the DeFi world may seem necessary.

Transparency. Transparency is another alternative, which seems more desirable. Many CEXes already created proof of reserves of assets as evidence delivered to the public. However, the proof of reserve cannot reflect the full picture of exchange solvency such as the liabilities. CEXes and CeFi-related tools need to rely on external forces to restore markets’ confidence. In contrast, DeFi protocols naturally inherit a series of advantages of on-chain transparency, selfcustody&governance, and fair access for participants [25]. The logic and rules written in smart contracts are fully transparent that can be publicly checked by anyone. But it still is not an ideal solution due to its high security risks. Any logic error or loop bugs will be continuously running until the system crashes. Abilities on self-calibrating&correcting are absent. Thus prior security audits are of particular importance to DeFi protocols.

5 Concluding Remarks

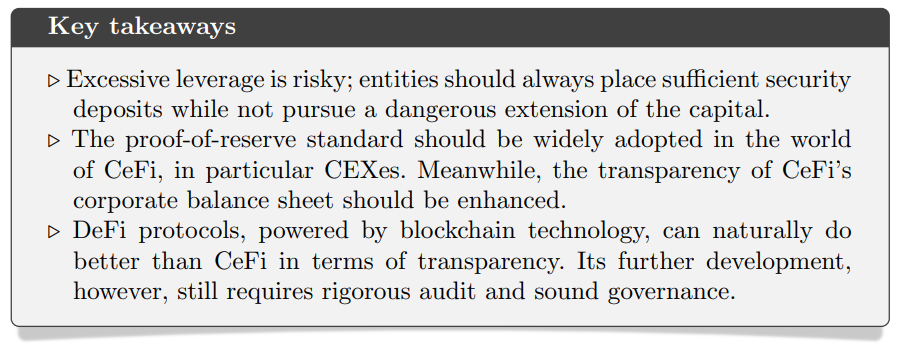

In this paper, we dig into the root reasons for FTX collapse. By comparing it with a rational Ponzi model, we identify major violations that break the game rules and as a result, lead to the final crash. Although there are possible ways to avoid similar disasters, none are without their flaws. Further endeavors are required for establishing sustainable token ecosystems. At last, we deliver three pieces of home-taking messages as summaries.

References

-

CoinMarketCap. Cryptocurrency Prices, Charts And Market Capitalizations —CoinMarketCap, 2022. [Online; accessed 19-Nov-2022].

-

CoinDesk. Divisions in Sam Bankman-Fried’s Crypto Empire Blur on His Trading Titan Alameda’s Balance Sheet. https://www.coindesk.com/business/2022/11/02/divisions-in-sam-bankman-frieds-crypto-empire-blur-on-his-trading-titan-alamedas-balance-sheet/, 2022.

-

Khaitan Tarang. Solana endures ‘crucible’ as ftx connection deletes 70% of tv. Accessible at https://thedefiant.io/solana-test-ftx-crisis, 2022.

-

Gilbert Aleksandar. Ftx-backed bitcoin and ether tokens depeg on solana. Accessible at https://thedefiant.io/ftx-files-for-bankruptcy, 2022.

-

Shumba Camomile. Us justice department wants ftx fraud allegations to be investigated. Accessible at https://www.coindesk.com/policy/2022/12/02/us-justice-department-wants-ftx-fraud-allegations-to-be-investigated/.

-

Vogelsteller Fabian and Buterin Vitalik. Erc-20 token standard. https://ethereum.org/en/developers/docs/standards/tokens/erc-20/.

-

Gavin Wood et al. Ethereum: A secure decentralised generalised transaction ledger. Ethereum yellow paper, 151(2014):1–32, 2014.

-

Kaushik Basu. The ponzi economy. Scientific American, 310(6):70–75, 2014.

-

Sam M Werner, Daniel Perez, Lewis Gudgeon, Ariah Klages-Mundt, Dominik Harz, and William J Knottenbelt. Sok: Decentralized finance (defi). arXiv preprintarXiv:2101.08778, 2021.

-

Khoo Yong Li, Leow Sandra, Choe Louisa, Polk Niklas, and Chia Douglas. Blockchain analysis: The collapse of alameda and ftx. Accessible at https://www.nansen.ai/research/blockchain-analysis-the-collapse-of-alameda-and-ftx, 2022.

-

Dalia Ramirez. Ftx crash: Timeline, fallout and what investors should know. https://www.nerdwallet.com/article/investing/ftx-crash, 2022.

-

Jakub. Ftx collapse – what is the path forward for crypto. https://finematics.com/the-ftx-collapse-explained/, 2021.

-

CoinDesk. The FTX Downfall: Full Coverage – Follow the key developments of the unraveling of Sam Bankman-Fried’s crypto empire and exchange, FTX. Accessible at https://www.coindesk.com/ftx-news-coverage/, 2022.

-

Nathan, Reiff and Vikki, Velasquez. The Collapse of FTX: What Went Wrong with the Crypto Exchange? https://www.investopedia.com/what-went-wrong-with-ftx-6828447, 2022.

-

Forbes. The Collapse Of FTX. https://www.forbes.com/sites/forbesstaff/article/the-fall-of-ftx/?sh=14bbd 8aa7d0c, 2022.

-

Wikiwand. Bankruptcy of ftx. https://www.wikiwand.com/en/Bankruptcy of FTX , 2022.

-

Fernau Owen. Crypto users jump to defi platforms in wake of ftx’s cefi crash. Accessible at https://thedefiant.io/defi-surge-ftx-crash.

-

Fernau Owen. Stablecoins show signs of stabilizing after ftx storm. Accessible at https://thedefiant.io/stablecoins-show-signsof-stabilizing-after-ftx-storm.

-

Investor.gov U.S. SECURITIES AND EXCHANGE COMMISSION. Ponzi Scheme, 2022. [Online; accessed 19-Nov-2022].

-

Stephen A O’Connell and Stephen P Zeldes. Rational ponzi games. International Economic Review, pages 431–450, 1988.

-

Shange Fu, Qin Wang, Jiangshan Yu, and Shiping Chen. Rational ponzi games in algorithmic stablecoin. arXiv preprint arXiv:2210.11928, 2022.

-

Olivier J Blanchard and Philippe Weil. Dynamic efficiency, the riskless rate, and debt ponzi games under uncertainty. National Bureau of Economic Research Cambridge, Mass., USA, 1992.

-

Wiki. Pareto efficiency. Accessible at https://www.wikiwand.com/en/Pareto_efficiency, 2021.

-

PitchBook. PitchBook Profile – FTX, 2022. [Online; accessed 19-Nov-2022].

-

Kaihua Qin, Liyi Zhou, Yaroslav Afonin, Ludovico Lazzaretti, and Arthur Gervais. Cefi vs. defi–comparing centralized to decentralized finance. Crypto Valley Conference on Blockchain Technology (CVCBT), 2021.

-

Marshall Van Alstyne. Why bitcoin has value. Communications of the ACM, 57(5):30–32, 2014.

-

George T McCandless, Warren E Weber, et al. Some monetary facts. Federal Reserve Bank of Minneapolis Quarterly Review, 19(3):2–11, 1995.

:::info

Authors:

(1) Shange Fu, Monash University, Australia;

(2) Qin Wang, CSIRO Data61, Australia;

(3) Jiangshan Yu, Monash University, Australia;

(4) Shiping Chen, CSIRO Data61, Australia.

:::

:::info

This paper is available on arxiv under CC BY 4.0 DEED license.

:::

{kind=link}