Table of Links

Abstract and 1. Introduction

2. Data and quantitative nature of the events

2.1. Hourly data analysis

2.2. Transaction data analysis

2.3. Anchor protocol

3. Methodology

3.1. Network analysis: Triangulated Maximally Filtered Graph (TMFG)

3.2. Herding analysis

4. Results

4.1. Correlations and network analysis

4.2. Herding analysis: CSAD approach

5. Robustness analysis

6. Implications and future research

6.1. Relevance for stakeholders

6.2. Future lines of research

7. Conclusion, Acknowledgements, and References

Supplementary Material

5. Robustness analysis

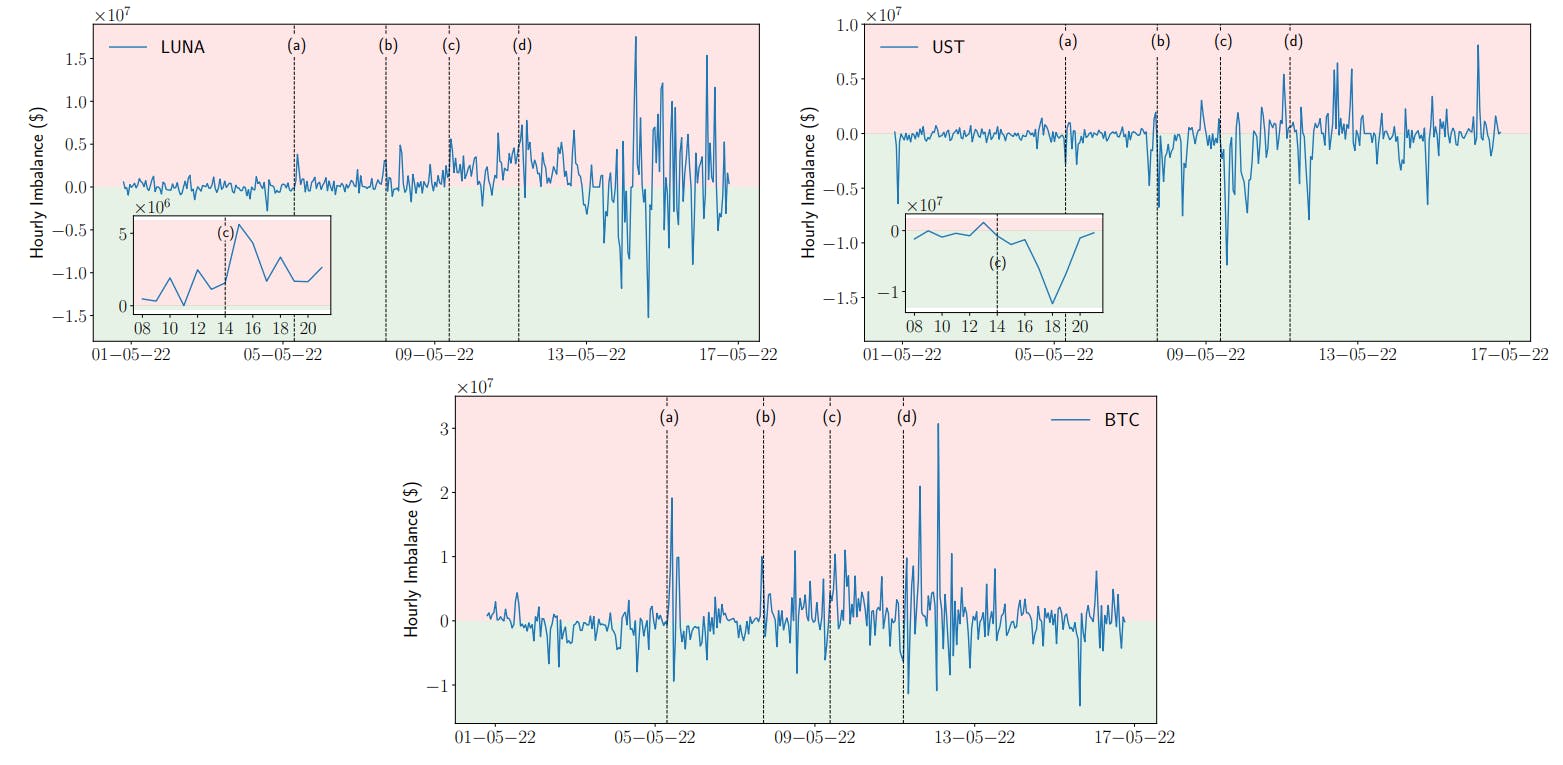

In this section, we use data from Binance digital currency exchange (the largest digital currency exchange platform according to CoinMarketCap (2022b)) to assess the robustness of our results. Data retrieving is entirely accomplished

using the CCXT (Ccxt, 2022) Python package. Compared to Kraken, Binance’s cross-rates are expressed in BUSD (BinanceUSD), which could give rise to some inconsistencies in comparative studies (see e.g. Alexander and Dakos, 2020). Consequently, we use it only in the context of robustness analysis. For the sake of space, we only report results where we observe more significant differences (see Figure 8). The rest of the results are consistent with the ones observed in Kraken and are available upon request. In Figure 8 we show two relevant findings. First, in line with Kraken (see Figure 2), on 05 May 2022 (a), we identify a high positive imbalance for BTC, which is remarkably lower only than a peak after the Terra project’s collapse. This result enforces the finding that if short-selling positions were opened against BTC, this potentially happened on 05 May 2022. Second, focusing on UST, contrary to what observed on Kraken, we find a considerable degree of buying pressure during the Terra project’s collapse. This finding could imply that Binance was used by LFG and/or other market actors to defend the UST peg.[16]

6. Implications and future research

6.1. Relevance for stakeholders

Considering that the failure of large stablecoins built upon inappropriate decentralized finance frameworks (e.g. lack of collateral and dependencies with liquidity providers) could give rise to potential financial stability risks, we believe that our results are relevant for both investors and policymakers. Applications of stablecoins within the crypto space remarkably increased since 2020, while poorly supported by adequate regulation. Initially, they were used as: (i) bridge between fiat currencies and crypto-assets; (ii) “parking space” for crypto volatility (Adachi et al., 2022). Nowadays, they are also used to provide most of the liquidity in DeFi applications such as decentralised exchanges and lending protocols (e.g. UST and Anchor protocol). Consequently, stablecoins play a critical role within the crypto space, where they are involved in almost 75% of the entire trading (Adachi et al., 2021). Largest stablecoins represent a primary source of risk according to the European Central Bank (ECB), which states that a “bank run” on Tether could disrupt trading and price discovery in crypto-asset markets, which could turn disorderly (ECB, 2022). Therefore, even though the collapse of UST was not able to rise relevant herding effects, the failure of larger stablecoins could generate systemic effects on the whole crypto universe. In addition, considering the growing interlinks between crypto-assets and the traditional financial system, the failure of stablecoins could also have implications external to the crypto space. These scenarios remark the need for a Global Stablecoin Standard and continuously updated regulations able to guarantee (i) a process for fulfilling holders’ redemption claims, (ii) proper transparency of reserve asset composition and (iii) development of appropriate risk-management frameworks. Relevant regulatory standard-setting bodies (Financial Stability Board and Bank of International Settlements; see, e.g. Bank for International Settlements, 2022) and governments (Japan, Hong Kong, United Kingdom, European Union and the United States; see, e.g. Asmakov, 2022, European Council, 2022) are already proposing robust rules for these digital assets. It would be beneficial that contributions from inside the DeFi community would also be proposed.

6.2. Future lines of research

Most of the existing literature on stablecoins concerns their stability (Grobys et al., 2021), their role in portfolio diversification (Wang et al., 2020; Baur and Hoang, 2021), and crypto asset price formation (Barucci et al., 2022; Kristoufek, 2022). Due to the nascent interest in this research field and the rapid growth of decentralised finance, gaps in the literature still exist. Recent events around Terra project highlights the need to analyse specific topics that have been neglected until now: (i) stablecoins as a means of exchange, (ii) stablecoins’ role within the crypto space, (iii) regulation on stablecoins and related protocols and (iv) potential risk to financial stability. First, stablecoins could not be appropriate as a mean of exchange due to their vulnerability to “bank runs” and high transaction costs compared to non-blockchain alternatives (Mizrach, 2022). Second, the role of stablecoins as “bridge” in the crypto space could be considered a double-edged sword since they could jeopardise the system’s stability once becoming systemic. Third, the dependence of UST on Anchor protocol remarks the need for better scrutiny of third party protocols related to any stablecoin. Finally, it would be necessary to consider scenarios in which specific fragilities within the stablecoins’ ecosystem may give rise to systemic financial stability risks.

7. Conclusion

In this paper, we review the Terra project’s main features and describe the mechanisms that led to its failure. Our contribution to the existing literature is threefold. We first systematically organise news from heterogeneous sources to reconstruct a reliable timeline for the Terra project’s collapse. We hence identify four main breakpoints for the crash and, starting from hourly data for 61 cryptocurrencies from Kraken digital currency exchange, we quantitatively characterise them. We exploit the power of smoothed weighted correlations to build state-of-the-art graph structures which demonstrate to be both able to efficiently capture dependency structures among cryptocurrencies and robust to extreme market conditions. As a further element of novelty, we enforce our analysis using transaction data to detect relevant micro-structural market events.

Combining these last two approaches, we uncover BTC’s reference role during the first phase of the collapse. In particular, we outline the existence of intense selling pressure on this crypto asset and identify 05 May 2022 as the potential fuse for the process that led to the Terra project’s failure. We remark that it is impossible to conclude that this event and the Terra project’s collapse were part of a coordinated strategy (del Castillo, 2022). The weakness of the current global economy (e.g. Russia – Ukraine conflict (Boungou and Yati´e, 2022), bear markets in the main financial indices (Krauskopf, 2022), and higher federal funds rates (Cox, 2022)) could have caused “the perfect storm” in the cryptocurrency market. Moreover, it is relevant to consider that the vicious dependence of the Terra project on the Anchor protocol could have increased its exposure to heterogeneous speculative strategies that occurred simultaneously by chance. We also show how, after 07 May 2022, LUNA is quickly marginalised by the rest of the network’s components. This last finding enforces the conjecture that investors considered this collapse a non-structural shock, which is supported by the impossibility of detecting a herding behaviour during the down market.

Finally, to prove our results’ robustness, we compare buy/selling dynamics detected on Kraken digital currency exchange with those detected on Binance, highlighting how adverse market actors could have used multiple exchanges to attack/defend the Terra ecosystem.

Acknowledgements

The author, A.B. acknowledges Dr. Silvia Bartolucci for her precious support in data retrieving. The author, D.VT., acknowledges the financial support from the Margarita Salas contract MGS/2021/13 (UP2021-021) financed by the European Union-NextGenerationEU. The author, T.A, acknowledges the financial support from ESRC (ES/K002309/1), EPSRC (EP/P031730/1) and EC (H2020-ICT-2018-2 825215). All the authors acknowledge Cryptocompare for easing the data access. All the authors acknowledge Miranda Zhang for her help in producing graphical representations.

References

Adachi, M., Born, A., Gschossmann, I., and Van der Kraaij, A. (2021). The expanding functions and uses of stablecoins. Financial Stability Review (ECB).

Adachi, M., Pereira Da Silva, P. B., Born, A., Cappuccio, M., Cz´ak-Ludwig, S., Gschossmann, I., Paula, G., Pellicani, A., Philipps, S.-M., Mirjam, P., Rossteuscher, I., and Zeoli, P. (2022). Stablecoins’ role in crypto and beyond: functions, risks and policy. European Central Bank.

Alexander, C. and Dakos, M. (2020). A critical investigation of cryptocurrency data and analysis. Quantitative Finance, 20(2):173–188.

Anchor (2022). Anchor protocol Dashboard. https://app.anchorprotocol.com/.

Anchor Forum (2022). Dynamic Anchor Earn Rate. https://forum.anchorprotocol.com/t/dynamic-anchor-earn-rate/3042.

Anchor Protocol (2021). 1/ we’re thrilled to present anchor. Twitter. https://twitter.com/anchor protocol/status/1372140667669938180.

Ashmore, D. (2022). What happened ust, and was it an attack? Invezz. 11 May.

Aslanidis, N., Bariviera, A. F., and Perez-Laborda, A. (2021). Are cryptocurrencies becoming more interconnected? Economics Letters, 199:109725.

Asmakov, A. (2022). Japan passes stablecoin bill aimed at protecting crypto investors. Decrypt.

Aste, T. (2022). Topological regularization with information filtering networks. Information Sciences, 608:655–669.

Aste, T., Shaw, W., and Di Matteo, T. (2010). Correlation structure and dynamics in volatile markets. New Journal of Physics, 12(8):085009.

Bank for International Settlements (2022). Application of theprinciples for financial market infrastructures tostablecoin arrangements. Technical report. 22 July 2022.

Barucci, E., Marazzina, D., and Giuffra Moncayo, G. (2022). A deep dive into crypto-markets: we cannot compare oranges with apples. Working paper. See UCL – Financial Computing and Analytics seminar: https://www.youtube.com/watch?v=-cOKdja1BuE.

Baur, D. G. and Hoang, L. T. (2021). A crypto safe haven against bitcoin. Finance Research Letters, 38:101431.

Bonato (2022). TerraLuna & UST – Risk Assessment. https://hubs.ly/Q017Ww2S0.

Boungou, W. and Yati´e, A. (2022). The impact of the ukraine–russia war on world stock market returns. Economics Letters, 215:110516.

Briola, A. and Aste, T. (2022). Dependency structures in cryptocurrency market from high to low frequency.

Calcaterra, C., Kaal, W. A., and Rao, V. (2020). Stable cryptocurrencies: First order principles. Stan. J. Blockchain L. & Pol’y, 3:62.

Ccxt (2022). Ccxt – cryptocurrency exchange trading library. https://github.com/ccxt/ccxt.

Chainanalysis (2022). The trades that triggered ust’s collapse. Technical report. 9 June 2022.

Chang, E. C., Cheng, J. W., and Khorana, A. (2000). An examination of herd behavior in equity markets: An international perspective. Journal of Banking & Finance, 24(10):1651–1679.

Chiang, T. C. and Zheng, D. (2010). An empirical analysis of herd behavior in global stock markets. Journal of Banking & Finance, 34(8):1911–1921.

Christie, W. G. and Huang, R. D. (1995). Following the pied piper: Do individual returns herd around the market? Financial Analysts Journal, 51(4):31–37.

Clements, R. (2021). Built to fail: The inherent fragility of algorithmic stablecoins. Wake Forest L. Rev. Online, 11:131.

CoinMarketCap (2022a). Coinmarketcap: Historical data for terraclassicusd. Accessed: 2022-07-14, https://coinmarketcap.com/it/currencies/terrausd/historical-data/.

CoinMarketCap (2022b). Coinmarketcap: Top cryptocurrency spot exchanges. Accessed: 2022-07-14, https://coinmarketcap.com/it/rankings/exchanges/.

Cox, J. (2022). Fed hikes interest rates by 0.75 percentage point for second consecutive time to fight inflation. CNBC.

CryptoCompare (2022). Data from Cryptocompare, www.cryptocompare.com.

Cui, Y., Gebka, B., and Kallinterakis, V. (2019). Do closed-end fund investors herd? Journal of Banking & Finance, 105:194–206.

da Gama Silva, P. V. J., Klotzle, M. C., Pinto, A. C. F., and Gomes, L. L. (2019). Herding behavior and contagion in the cryptocurrency market. Journal of Behavioral and Experimental Finance, 22:41–50.

del Castillo, M. (2022). Blackrock and citadel deny trading cratering stablecoin. Forbes. May11.

ECB, D. G. M. P. . F. S. (2022). Market sensitivity to pace of policy normalisation. Financial Stability Review.

European Council (2022). Digital finance: agreement reached on european crypto-assets regulation (mica). Technical report. 22 July 2022.

Finematics (2021). Bank run in defi – iron finance fiasco explained. Technical report. 9 June 2022.

Fratianni, M. and Artis, M. J. (1996). The lira and the pound in the 1992 currency crisis: Fundamentals or speculation? Open economies review, 7(1):573–589.

Grobys, K., Junttila, J., Kolari, J. W., and Sapkota, N. (2021). On the stability of stablecoins. Journal of Empirical Finance, 64:207–223.

Hall, J. (2022). Luna meltdown sparks theories and told-you-sos from crypto community. Cointelegraph. 11 May.

Iron Finance (2021a). Iron finance post-mortem. Technical report. 17 June 2021.

Iron Finance (2021b). our apy is way higher. you are still showing apr :). Twitter.

Jung, C. (2022). Earn 20Medium. 17 February.

Kelly, L. J. (2022). We need to talk about terra’s anchor. Decrypt.

Kereiakes, E., Do Kwon, M. D. M., and Platias, N. (2019). Terra money: Stability and adoption. White Paper, Apr.

Krauskopf, L. (2022). Bear market confirmed as u.s. stocks’ 2022 descent deepens. Reuters.

Kristoufek, L. (2022). On the role of stablecoins in cryptoasset pricing dynamics. Financial Innovation, 8(1):1–26.

Kwon, D. (2022a). 1/ dear terra community. Twitter. https://twitter.com/stablekwon/status/1524331171189956609.

Kwon, D. (2022b). 1/ introducing the 4pool. Twitter. https://twitter.com/stablekwon/status/1510021707377287170.

Locke, T. (2022). Did a ‘concerted attack’ cause terra’s ust to crash below $1? an exec behind the largest stablecoin and experts agree it’s suspicious. Fortune.

Luna Foundation Guard (2022). 1/ as of saturday, may 7, 2022. Twitter. https://twitter.com/LFG org/status/1526126703046582272.

Mantegna, R. N. (1999). Hierarchical structure in financial markets. The European Physical Journal B-Condensed Matter and Complex Systems, 11(1):193–197.

Massara, G. P., Di Matteo, T., and Aste, T. (2017). Network filtering for big data: Triangulated maximally filtered graph. Journal of complex Networks, 5(2):161–178.

Messari (2022). Messari: Messari crypto research, data, and tools. Accessed: 2022-07-19, https://messari.io.

Mizrach, B. (2022). Stablecoins: Survivorship, transactions costs and exchange microstructure. arXiv preprint arXiv:2201.01392.

Morris, D. Z. (2022). There was no terra ‘attack’. Coindesk. 11 May.

Newey, W. K. and West, K. D. (1994). Automatic lag selection in covariance matrix estimation. The Review of Economic Studies, 61(4):631–653.

Platias, N., Lee, E. J., and Di Maggio, M. (2020). Anchor: Gold standard for passive incomeon the blockchain.

Pozzi, F., Di Matteo, T., and Aste, T. (2012). Exponential smoothing weighted correlations. The European Physical Journal B, 85(6):1–21.

Quiroz-Gutierrez, M. (2022). Who is do kwon, the ‘lunatic’ who created a $60 billion cryptocurrency that collapsed in days? Fortune. May 18.

Shapovalov, V., Hays, D., Kravchenko, I., Rosenberg, H., Valentin, A., Malkin, N., and Mendoza, R. (2022). Terra luna: Can digital assets boost the e-commerce market? Technical report, Cointelegraph.

Vidal-Tomas, D. (2022). Which cryptocurrency data sources should scholars use? International Review of Financial Analysis, 81:102061.

Wang, G.-J., Ma, X.-y., and Wu, H.-y. (2020). Are stablecoins truly diversifiers, hedges, or safe havens against traditional cryptocurrencies as their name suggests? Research in International Business and Finance, 54:101225.

Supplementary Material

List of the 61 cryptocurrencies analysed in the current paper. For each asset, the symbol, the name and the corresponding sector according to the taxonomy proposed by Messari (2022) is reported. There is no consensus on a unique mapping between cryptocurrencies and sectors. The chosen taxonomy is the one adopted by Kraken digital currency exchange.

Authors:

(1) Antonio Briola, Department of Computer Science, University College London, Gower Street, WC1E 6EA – London, United Kingdom and UCL Centre for Blockchain Technologies, London, United Kingdom;

(2) David Vidal-Tomas (Corresponding author), Department of Computer Science, University College London, Gower Street, WC1E 6EA – London, United Kingdom, Department of Economics, Universitat Jaume I, Campus del Riu Sec, 12071 – Castellon, Spain and UCL Centre for Blockchain Technologies, London, United Kingdom ([email protected]);

(3) Yuanrong Wang, Department of Computer Science, University College London, Gower Street, WC1E 6EA – London, United Kingdom and UCL Centre for Blockchain Technologies, London, United Kingdom;

(4) Tomaso Aste, Department of Computer Science, University College London, Gower Street, WC1E 6EA – London, United Kingdom, Systemic Risk Centre, London School of Economics, London, United Kingdom, and UCL Centre for Blockchain Technologies, London, United Kingdom.

[16] In the case of LUNA, we observe high instability since 13 May 2022, which could be caused by speculators trading when the price was close to 0 or by the run to positions’ liquidation.

{kind=link}