:::info

Authors:

(1) Shange Fu, Monash University, Australia;

(2) Qin Wang, CSIRO Data61, Australia;

(3) Jiangshan Yu, Monash University, Australia;

(4) Shiping Chen, CSIRO Data61, Australia.

:::

Table of Links

Abstract and 1. Introduction

2. What is Ponzi?

3. The FTX Collapse

4. Future Directions

5. Concluding Remarks and References

Abstract. FTX used to be the third-largest centralised exchange (CEX) in crypto markets, managing over $10B in daily trading volume before its downfall. Such a giant, however, failed to avoid the fate of mania, panic, and crash. In this work, we revisit the FTX’s crash by telling it as a Ponzi story. In regards to why FTX could not sustain this Ponzi game, we extract and demonstrate the three facilitators of the FTX collapse, namely, FTT , leverage, and diversion. The unfunctionality in each factor can iteratively magnify the impact of damages when the panic is triggered. Rooted in the unstable ground, FTX eventually suffered insolvency and rapidly crashed in Nov. 2022. The crisis of FTX is not an isolated event; it consequently results in the collapse of a chain of associated companies in the entire crypto market. Recall this painful experience, we discuss possible paths for a way forward for both CeFi and DeFi services.

1 Introduction

FTX, before collapsing, was the third-largest cryptocurrency exchange that handles over $10 active trading volume [1]. FTX was created by its founder Sam Bankman-Fried (SBF in short) in 2019 and experienced a skyrocketing development within three years. Besides this influential trading platform, SBF also created a hedge fund called Alameda Research that manages $14.6B assets ($6B from FTT [3] and other collateral while $8B liabilities [2]). However, FTX struck a deal for Binance and halted all non-fiat customer withdrawals. , FTX declared bankruptcy on Nov. 11, 2022, which marks the collapse of the entire empire. The negative impact rapidly spreads over entire financial markets. Most mainstream cryptocurrency prices have declined more than 30% within hours. A large number of crypto-projects suffer inevitable catastrophes due to their close connection with FTX (e.g., Solana [3] [4]). Many traditional finance agencies that have relevant trades, such as hedge funds, also confront a huge amount of monetary loss. U.S. Department of Justice and federal agencies thereby started to investigate the ins and outs of the crash [5].

Back to FTX’s origin, we can observe a common pattern used in crypto projects: issue non-collateral tokens (primarily in the forms of ERC-20 tokens [6] in Ethereum ecosystem [7]) without any backed-up assets. This phenomenon is also known as ICO (short for Initial Coin Offering) which was prevalent since 2017. Not surprisingly, FTX issued its native token FTT in 2019, raising a significant of high-liquidity crypto assets including BTC and ETH. However, such a design pattern implicitly inherits the Ponzi nature [8], in which the asset manager always borrows new money to pay off the old debts until the game collapses. Typically, the issuance of a new token is costless (equiv. without collateral).

The reasons behind the FTX collapse are not pioneering, though indeed it was facilitated in several innovative ways by DeFi protocols. In fact, apart from pure scams in crypto markets, many means from traditional financial markets have also been applied in today’s DeFi games as an add-on, with leverage being the most popular one. Rather than its classic connotation on financial derivatives like futures and options, leverage refers to the iterative magnification of the impacts of one type of created tokens (FTT in this paper). One FTT token can yield, perhaps, 100X or much more value after traveling across several centralised exchanges and DeFi protocols [9]. Another important factor is divert, referring to the misappropriation of reserves. In particular, current crypto-markets are absent of formal regulation, which has spawned many types of CeFi/DeFi services without rigorous background checks or authentication. There is an unbelievable fact that crypto-users, unfortunately, are keen on this kind of game due to its potential for extremely high-return. A similar story happens on FTX, and with a high probability, will happen repeatedly in the future. This motivates us to explore a series of decisive factors that may alter the ending of stories.

Contribution. We explore the reasons that cause FTX’s collapse by retelling the story in the context of the Ponzi model. We first present the fundamentals of Ponzi and, more importantly, a rational Ponzi game as the baseline of our explanation (Sec.2). Based on this theoretical model, we decompose three major phases of FTX’s growth and accordingly analyze the root reasons that break the game rules (Sec.3). We show that the failure of FTX is not an accident but, instead, caused by its severe violations against a rational model. Further, we provide discussion and advice on potential aspects, namely regulation and transparency, for future endeavors (Sec.4).

Related Work. Nansen [10] provides a research analysis that captures onchain data from May 2019 – Sep 2022, focusing on both FTT and Alameda activities. Ramirez [11] sorts out the timeline and milestones of the FTX crash. Jakub [12] aims to point out the future paths for centralised exchanges. Besides, many influential companies (e.g., CoinDesk [13], Investopedia [14]) and other mainstream media (e.g., Forbes [15], Wiki [16]), also put their focus on such a historical event by recalling, analysing, and summarising its ins and outs. However, most of the cryto-collapse research, reports, and posts [17] [18] (topics also covering LUNA-UST’s depeg) are based on facts and explicit data without the in-depth abstraction of easy-understanding models or insights, which is the key matter that we aim to deliver in this paper.

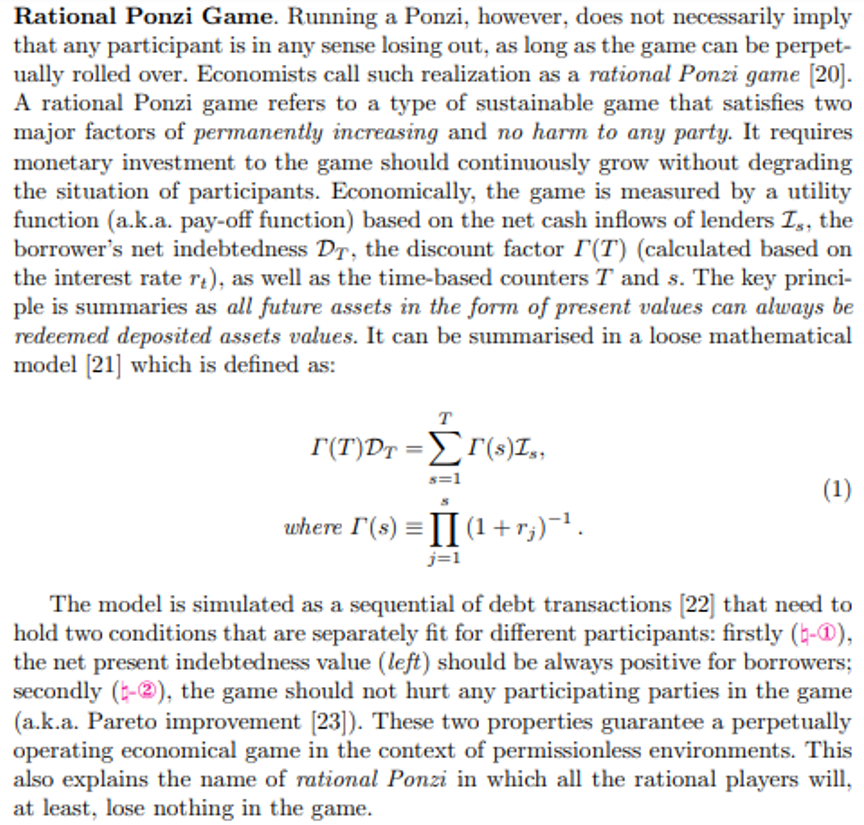

2 What is Ponzi?

The Ponzi game, commonly referred to as the Ponzi scheme, is named after Charles Ponzi, who duped investors in the 1920s with a postage stamp speculation scheme. Ponzi is essentially a financial protocol that old liability should be financed by issuing new debt. For those who are deliberately deceptive, Ponzi scheme organizers often promise to invest your money and generate high returns with little or no risk. But in practical Ponzi schemes, fraudsters do not invest money. Instead, they use it to pay those who invested earlier and may keep some for themselves. Ponzi schemes normally share common characteristics, and U.S. Securities and Exchange Commission [19] raises “red flags” for these warning signs: (i) high returns with little or no risk; (ii) overly consistent returns; (iii) unregistered investments; (iv) unlicensed sellers; (v) secretive, complex strategies; (vi) issues with paperwork; and (vii) difficulty receiving payments.

We then demonstrate how a Ponzi scheme works (and how it may be broken) in general in Fig.1. The green plus sign and the red minus sign represent cash inflows and cash outflows, respectively. The values in parentheses following each participant represent their corresponding utility. In a Ponzi scheme, the borrower or the issuer can always benefit from the game, and participants can reach a no-less-than-zero utility before the breaking of Ponzi, only the last wave of escapees will suffer losses. Therefore, a broken Ponzi scheme is a zero-sum game.

:::info

This paper is available on arxiv under CC BY 4.0 DEED license.

:::

[3] FTT is the native token of the crypto derivatives created by FTX that is launched on May 8, 2019. At the time of writing, FTX token price has dropped 62X from $79.53 (9/10/2021) to $1.29 (11/29/2022) [1].

{kind=link}