The cost of launching cargo into space was, for years, one of the great limits of the aerospace industry. LaNASA documents in several works, including the analyzes of Harry W. Jones, that during the last decades of the 20th century many launchers moved in a typical range between 10,000 and more than 20,000 dollars per kilowith an average cost of around $18,500/kg in low orbit, with the space shuttle far above due to its complexity and operating expense. It was not just the Price of the launch systems, but of a model based on disposable components, manual processes and highly specialized operations.

The situation remained stable for decades, until SpaceX decided to rethink how the economics of orbital launch should work. Instead of assuming these costs as inevitable, the company opted to reuse stages, optimize processes and manufacture its own engines and systems from scratch. This combination allowed the price per kilo to be reduced to unprecedented levels, although the change did not occur immediately. What is relevant is that, for the first time, a private actor demonstrated that launches could be much cheaper and that price did not have to be a structural barrier for the industry.

When launch is no longer the limit, attention shifts to satellites

The resulting prices began to change behavior in the sector. With Falcon 9 and Falcon Heavy, the cost per kilo became in the range of 3,000 to 1,500 dollarsaccording to NASA calculations based on catalog prices. These figures not only mark a reduction, but a turning point: for the first time, companies, institutions and even governments could rethink the design of missions knowing that launch was no longer the main economic barrier. From there a question arose that until then had no answer: if the trip had been made cheaper, what would happen to what was sent into space?

The traditional satellite model was built on the idea of optimizing each unit. It was not important to produce many, but to produce one that could operate for years, with high capacity and low probability of failure. Manufacturers and operators were investing in complex systems, with long development cycles, exhaustive testing and specialized structures to fulfill specific and prolonged missions. This strategy responded to an environment in which launch was so costly and infrequent that it was more profitable to prioritize reliability and durability than to think about scalability or rapid replenishment.

One of the first companies to help change this approach was OneWeb, which introduced a manufacturing model built for scale. Instead of ordering each satellite as an individual part, the company designed a common architecture and partnered with Airbus to produce repeatable units, with standardized processes and shorter manufacturing times. The plant installed in Florida in 2019 was presented as the first factory of satellite serial production on a large scale, with two lines capable of removing up to two units a day. It was not about building a better satellite, but about building many.

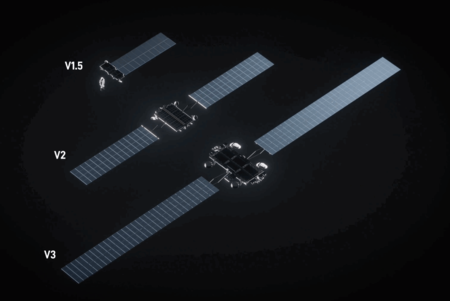

SpaceX took the satellite constellation idea and turned it into its own industrial system. With Starlink, it not only replicated the use of mass-produced satellites, but also linked that production to its launch capacity with Falcon 9, operated by the company itself. This integration allowed the deployment to be accelerated without depending on external release windows or commercial suppliers. The constellation began to grow at an unprecedented rate and, in a few years, it vastly surpassed any other similar project in number and pace. The difference was not only in manufacturing satellites, but in being able to launch them at will.

Although OneWeb was one of the first players to apply industrial logic to satellite manufacturing, its constellation has grown at a very different pace than Starlink. By the end of 2025, OneWeb has about 648 satellites in orbit, while SpaceX has more than 8,000 operational satellites, according to the most recent data published by orbital tracking firms. The difference is not only due to the number of launches, but also to the mode of production. According to an economic analysis published in 2025, the estimated manufacturing cost of OneWeb satellites is around $14,000 per kilo, compared to approximately $2,500 per kilo for Starlink satellites. These figures reflect a gap that has more to do with the integration model than with the technology itself.

The estimated manufacturing cost of OneWeb satellites is around $14,000 per kilo, compared to approximately $2,500 per kilo for Starlink satellites.

The reaction of the sector did not take long to arrive. With the advancement of Starlink, both companies and public institutions Similar projects began to be considered based on constellations with a high number of satellites and sustained deployments. Amazon launched Kuiper, Eutelsat and OneWeb reinforced their alliance to maintain a presence in the market and the European Union approved the IRIS2 program with institutional support. China is also working on its own large systems. It is not just about competing in numbers, but about accepting that scale and replacement capacity are part of the new spatial model.

When the satellite becomes a replicable product, the way of planning its presence in orbit also changes. It is no longer about launching a mission and hoping it works for as long as possible, but rather about building a structure that can grow, modernize and replace units regularly. The satellite becomes a component of a network, not the center of the mission. This logic favors models based on scalability and continuous replacement, similar to those of other technological infrastructures. Space stops being a destination and becomes a platform.

SpaceX demonstrated that the cost of the launch was not a technical limit, but rather a model one. Now it is trying to apply that same logic to satellites, with an approach based on scale, continuous manufacturing and integration with its own launch systems. The result is not only a larger constellation, but a different way of understanding what it means. operate in orbit. The question is no longer how much it costs to get to space, but who can sustain an infrastructure there. And in that conversation, SpaceX has become a relevant player.

Images | WorldOfSoftware with Gemini 3

In WorldOfSoftware | In a gesture of incalculable Frenchness, France has named the first rocket launched from its borders “Baguette One”

{kind=link}