It seems like a deal for long-term investors.

One of the top artificial intelligence (AI) stocks on the market isn’t one that the public interacts with. However, it plays perhaps the most important role in the AI supply chain. Are Taiwanese semiconductor manufacturing company (TSM +1.78%) (TSMC), the world’s largest semiconductor (chip) foundry.

Although companies like it Nvidia And AMD design chips for their hardware, TSMC is the one that actually produces them, turning blueprints into reality. Without TSMC, the AI supply chain would suffer. And while it continues to post impressive growth, it’s still trading at a discount in my opinion.

Image source: TSMC.

What sets TSMC apart?

When it comes to efficiency, scale, precision and yield (the percentage of chips that work as planned), TSMC’s capabilities are a step above those of its competitors.

Companies that need chips need reliability, otherwise their business could go bankrupt. TSMC is the most reliable company in the industry, and it is the go-to choice.

The company used to mainly make chips for smartphones, but now, amid the AI gold rush, it has found a lucrative avenue in making advanced AI chips for data centers. The market share for them is well into the upper 90% range.

Taiwanese semiconductor manufacturing

Today’s change

(1.78%)$5.91

Current price

$338.62

Key data points

Market capitalization

$1.7 tons

Day range

$334.63 -$339.30

Range of 52 weeks

$134.25 -$351.33

Volume

156K

Avg. full

13M

Gross margin

59.02%

Dividend yield

0.92%

TSMC’s best year yet

TSMC generated revenue of $122.4 billion in 2025, up nearly 36% from 2024. This was the first $100 billion year in TSMC history, and exceeded the mark with plenty of room to spare.

Just as impressive is TSMC’s margin growth over the past year. Gross margin increased from 56.1% to 59.9% in 2025, and operating margin increased from 45.7% to 50.8%. In the fourth quarter, gross margin and operating margin were 62.3% and 54%, respectively.

A huge revenue jump alongside noticeable margin expansion is a sign of TSMC’s operational execution over the past year. It also provides insight into the pricing power of TSMC, which has a virtual monopoly on advanced AI chips. If you’re essentially the only game in town, you can charge a premium for your services.

TSMC looks like good value

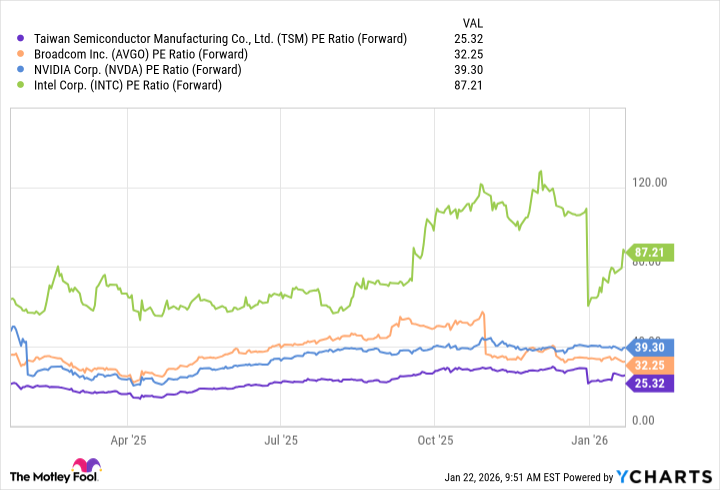

Although TSMC shares are up about 69% since the start of 2025 (as of January 22), they are trading at just 25 times expected earnings over the next year. This is much cheaper than semiconductor companies Broadcom, Inteland Nvidia.

TSM PE ratio (forward) data per YCharts

Given TSMC’s market dominance, pricing power, and growth opportunities, the current valuation seems like a deal for long-term investors. Trading is slightly higher than the average of recent years, but the company is also in a much better position now than it was for most of that time.

TSMC is a stock that I could confidently hold for the long term.

Stefon Walters has positions in Taiwan Semiconductor Manufacturing. The Motley Fool holds positions in and recommends Advanced Micro Devices, Intel, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Fool recommends Broadcom. The Motley Fool has a disclosure policy.

{kind=link}