Semiconductor stocks are among the biggest winners of the artificial intelligence (AI) revolution so far.

Wall Street’s obsession with artificial intelligence (AI) stocks has helped fuel a historic bull market in recent years. Megacap tech stocks in particular have witnessed a pronounced valuation boom during the AI revolution, which has contributed to some frothiness in the major indices.

As growth stocks rise, it becomes increasingly difficult to find a good deal in the market. However, I’ve found one AI stock that stands out from the rest in this regard.

Last year, shares of Micron technology (MU 2.64%) almost tripled. This performance only adds to the company’s illustrious shareholder returns. Since its initial public offering (IPO) in 1984, Micron’s shares have risen approximately 28,700%.

While it looks like Micron will be the market’s next momentum stock, I think the rally is just beginning. Let’s take a look at what makes Micron such an integral part of the AI ecosystem and analyze why its stock is about to go parabolic.

Image source: Micron Technology.

What does Micron do and why is it important for the development of AI?

When it comes to semiconductor stocks, smart investors understand that not all chips serve the same purpose.

Nvidia And Advanced micro devices design graphics processing units (GPUs) – the hardware on which generative AI models like ChatGPT are trained. On the other hand Broadcom helps the hyperscalers build custom silicon for specific workloads.

Micron operates in a completely different part of the chip landscape. The company specializes in high bandwidth memory and storage solutions. For much of its history, Micron has played an integral role in the consumer electronics market, often capitalizing on upgrade cycles in PCs and smartphones.

While Micron’s value proposition for the technology landscape was clear, the cyclical dynamics of consumer hardware were a blemish on the company’s growth potential. That story is rapidly changing thanks to the AI boom.

Micron’s business is booming

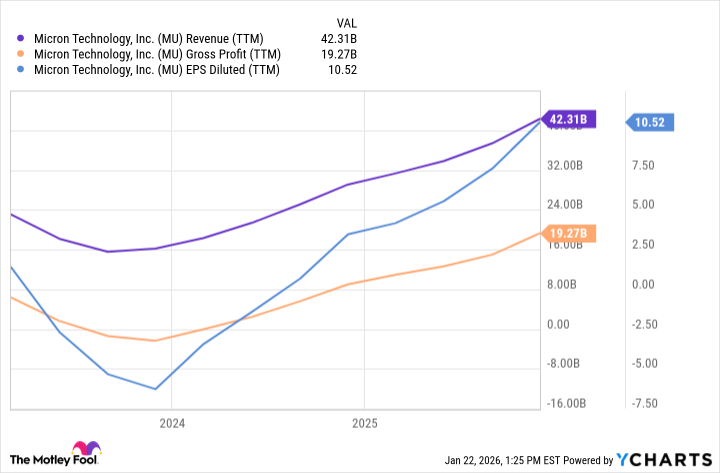

Over the past year, Micron’s revenues have kicked into new gear. This acceleration underlines that AI developers are starting to allocate larger portions of their capital expenditure budgets (capex) to memory and storage, rather than just GPU purchases.

MU Earnings Data (TTM) according to YCharts.

What’s even more impressive is the company’s ability to complement its revenue profile with improved profit margins. Considering that the total addressable market (TAM) for HBM chips is expected to grow at a compound annual growth rate (CAGR) of 40% and reach $100 billion by 2028, I suspect Micron will continue to witness rising sales and maintain healthy profits.

Micron shares are dirt cheap

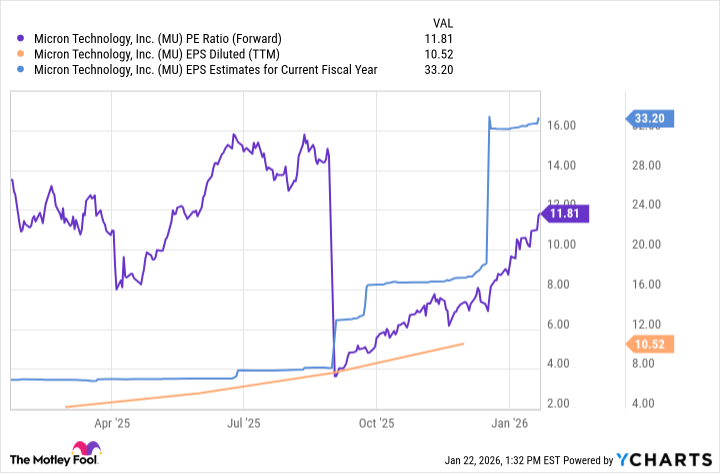

Over the past year, Micron generated about $10 in earnings per share (EPS). However, Wall Street’s consensus estimate for this year is $33.20. Nevertheless, Micron is currently trading at a rather ordinary price-to-earnings (P/E) ratio of 12.

MU PE ratio (forward) data according to YCharts.

Nvidia and Broadcom have achieved earnings multiples double and even triple compared to Micron. While these companies may not be direct competitors, the key takeaway is that the market has rewarded leaders in the broader chip value chain with premium valuations.

If Micron’s price-to-earnings ratio were to double, which I think is reasonable given the pace of its compound earnings profile, the stock could reach $780 per share by the end of the year – essentially implying a 100% upside from current prices.

In my view, Micron stock is the biggest buy in the AI infrastructure trade right now. I see the company as a no-brainer for investors with a long-term horizon.

{kind=link}