Few stocks are associated with artificial intelligence (AI) in this way. Nvidia is. The company has a dominant market share in the GPUs that are driving the AI industry. And if the AI market grows as fast as expected in the long term, it’s hard not to see Nvidia as a big winner.

But there’s a problem: Nvidia’s market cap is already approaching $3 trillion. While there may be plenty of growth ahead, the company probably won’t be able to keep up the pace of the past few years. After all, it will be significantly harder for Nvidia to double its $96 billion in annual revenue from a year ago, when it was $45 billion.

If you want to maximize your growth potential when betting on AI, you’ll want to look to smaller competitors. Fortunately, there’s a much smaller company to consider, one that Nvidia has invested nearly $4 million of its own funds into over the past year. Now’s your chance to follow Nvidia’s lead.

This AI stock has significant upside potential

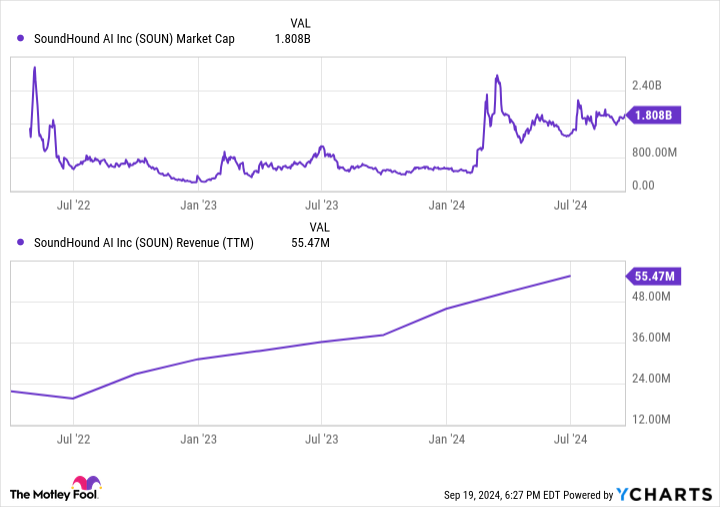

With a market cap of just $1.8 billion at the time of writing, it’s not hard to see significant upside potential in SoundHound AI (NASDAQ: SOUND). As the name suggests, SoundHound has developed a portfolio of AI technologies related to speech applications. Five Guys and Papa John’sFor example, have signed up as customers to use SoundHound’s speech recognition and natural language processing software to save costs and improve the phone ordering experience. Hyundai and Dodge have also signed agreements to integrate the technology into their vehicles, allowing drivers to chat with their cars about directions, messages and maintenance issues. Companies such as Snap And Visionhave since used SoundHound’s AI software to improve the customer experience of their own products.

Market estimates vary widely, but the total addressable market for speech and voice recognition software is valued at a minimum of $16 billion today, according to Fortune Business Insights. Still, future growth is expected to be extremely high, with demand expected to grow by at least 20% per year over the next decade. By 2032, the market could be worth around $85 billion. Compared to SoundHound’s $55 million revenue base, the upside potential is clear.

SoundHound has leveraged its technology portfolio, backed by more than 200 patents, to win dozens of new customers across a wide range of industries in recent years. Whether the customer is piloting the technology or fully implementing it, these customer additions have reputational benefits and also give SoundHound more data to train its AI models. In the second quarter, revenue grew 54% year-over-year. And based on market forecasts, SoundHound’s growth journey may just be getting started. There are, however, a few risks investors should be aware of.

Don’t go all-in on SoundHound

SoundHound has a lot of growth potential and an early-mover advantage, but it’s far from certain that the company will be a major player in the industry in a few years. Part of that is its size. The company’s relatively small revenue base of $55 million is barely enough for it to generate a profit.

The company lost $37 million last quarter, its biggest loss in years. This lack of profitability limits its ability to deploy capital, especially in critical areas such as research and development. Last quarter, research and development spending was just $16 million, the same level of spending the company reported three years ago.

As a result, SoundHound’s small size presents both opportunities and risks. It offers investors a lot of potential, but it also limits the company’s ability to invest in its technology, something its better-financed competitors appreciate. IBM And Alphabet I have no problem with it.

If SoundHound can maintain or grow its market share over the next few years, it should be able to ride the wave of rising AI spending. In this scenario, investors would likely win big. But if it falls behind deeper-pocketed competitors, there could be significant downside from here, especially considering that shares trade at nearly 25 times revenue.

Aggressive growth investors looking for multibagger return potential should bypass Nvidia and look at SoundHound. But even then, SoundHound stock should only comprise a small portion of your portfolio.

Should You Invest $1,000 in SoundHound AI Now?

Before you buy shares in SoundHound AI, you should consider the following:

The Motley Fool Stock Advisor team of analysts has just identified what they think is the 10 best stocks for investors to buy now… and SoundHound AI wasn’t one of them. The 10 stocks that made the cut could deliver monster returns in the years to come.

Think about when Nvidia made this list on April 15, 2005… if you had $1,000 invested at the time of our recommendation, you would have $710,860!*

Stock Advisor offers investors an easy-to-follow blueprint for success, including portfolio building guidance, regular analyst updates, and two new stock picks each month. The Stock Advisor has service more than quadrupled the return of the S&P 500 since 2002*.

View the 10 stocks »

*Stock Advisor returns as of September 23, 2024

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Ryan Vanzo has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Alphabet and Nvidia. The Motley Fool recommends International Business Machines. The Motley Fool has a disclosure policy.

Forget Nvidia: These Are My Best Artificial Intelligence (AI) Stocks to Buy Instead was originally published by The Motley Fool