You open the bank’s app, choose “Transfer,” you go, you write the name of the recipient and confirm. Today, October 7, 2025, if that name does not match the holder of the account, the usual thing is that the payment is executed without alerts. As of October 9, that everyday gesture changes. In the EU, starting with the entities of the euro area, the bank must check if the name you enter with that of the IBA before authorizing the shipment. The idea is simple, that money reaches who owes.

Until now, European banks were not obliged to verify whether the beneficiary’s name coincided with the IBA before executing a transfer. The system was based only on the account number, which allowed payments to be processed even if the name was not correct. Some countries, such as the Netherlands, had developed verification mechanisms such as the “Iran-Naam Check”, but there was no common norm. The new European regulation corrects that disparity and establishes a uniform procedure for the entire Union.

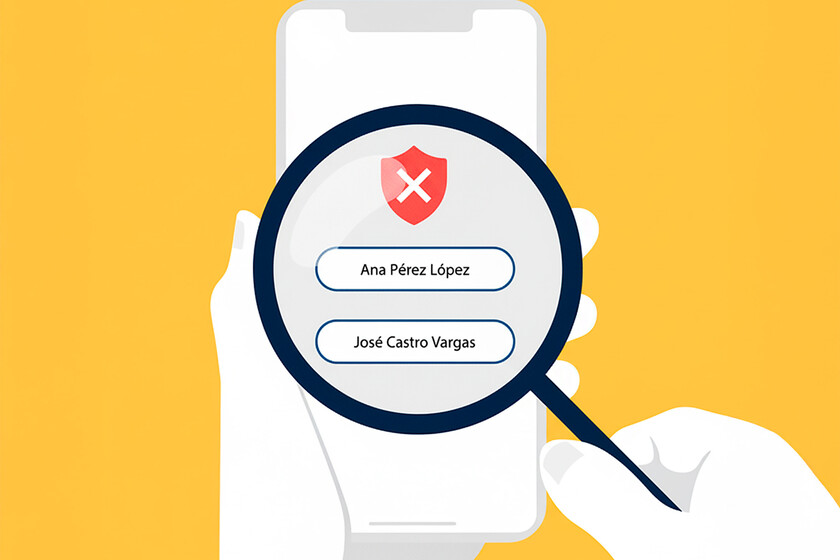

Three possible messages. When the bank taught the name and the Iban, the answer may be one of three.

- Total coincidence. If the data fully coincide, the transfer will be validated without additional notices.

- Partial coincidence. If there are slight differences (a changed letter, an absent tilde or an abbreviated name) an alert will appear indicating partial coincidence. In that case, the user may review the data or continue under their responsibility.

- Without coincidence. If there is no coincidence, the system will warn that the data does not quote, without showing the real name of the holder for privacy reasons.

WARNING, DO NOT BLOCK. Receiving an alert does not mean that the payment is blocked. The system is designed to inform, not to prevent the operation. Even if the name and the IBAN do not coincide, the user will be able to move forward with the transfer under their own responsibility. What changes is the transparency of the process. Before it was not known if the data fit; Now the bank will show you before executing the shipment. The final decision will remain yours.

People and companies. The verification is based on the identification data of the account holder. If the beneficiary is a natural person, the system will compare its name and surname as it appears in the receiving bank. In the case of a legal person (for example, a company or association), the verification will focus on the company name or the commercial name. The usual errors, such as tildes, abbreviations or second denominations, can generate partial coincidences, but will not prevent the transfer, as we mentioned above.

Standard, immediate and periodic. Verification will apply to both standard and immediate transfers, without additional cost for the user. One of the payment entities that have detailed how the process will work is Nickel. As explained, periodic transfers scheduled before October 9, 2025 will not be subject to the beneficiary’s check, even if their execution is subsequent. Only the coincidence in the new orders created from that date and once, at the time of configuring them, will be verified.

Absence of verification. As Nickel also explains, it can happen that the system fails to check the name with the Iban. This ruling, the company points out, may be due to communication problems between banks or specific technical limitations. In that case, the entity indicates that it will also proceed with the transfer, without the system confirming the coincidence of the beneficiary. Nickel herself advises to cancel the operation if there are doubts about the recipient, especially when it comes to high amounts or unusual accounts.

The origin of the measure is in the rebound of bank fraud in the last decade. The European institutions, headed by the Commission and the ECB, considered that the system knows a mechanism for verifying the beneficiary to prevent erroneous payments and identity robberies. With the new standard, each transfer will include an automatic verification that acts as an informative filter. It does not delay shipping, but offers a warning that did not exist before.

Vishing, smishing, romance y BEC. Behind the regulatory change are the fraud that proliferate in Europe and that banks try to stop new verification tools. Vishing, for example, uses false telephone calls to impersonate bank employees or authorities. Smishing arrives by SMS with messages that simulate being from the bank or a shipping company. Romantic scams have also extended, where the victim’s confidence is gained before asking for money, and CEO fraud, in which an alleged manager orders urgent and confidential transfers.

Beyond the differences between modalities, almost all bank scams share the same pattern. They use psychological manipulation techniques to generate urgency, fear or trust, and rely on identity supplant to seem legitimate. In most cases, they seek to make the user a bank transfer, taking advantage of emotions such as concern, empathy or hierarchical pressure. The verification of the beneficiary does not eliminate these risks, but it can act as a pause that allows to detect the deception in time.

Before clicking “Send.” Stop for a few seconds can make a difference. Before confirming a transfer, it is convenient to calmly review the name and I went from the recipient, especially if it is a new account or a recent change. If the bank notice indicates a partial or without coincidence, the most prudent is to verify the data by a different channel (a direct call or an official website). And, given the minimal suspicion, canceling is always better than regretting.

The new system also reaches companies and professionals who make frequent payments. Each transfer will require confirming the coincidence between the name of the beneficiary and the IBAN, which will add a small step to the usual process. For companies, it can be an opportunity to reinforce their treasury controls and detect internal fraud attempts or supplier supplant. It is not a lock, but a filter of verification.

What banks, what countries, what deadlines. The verification of the beneficiary will be mandatory for all payment service providers established in the European Union that manage transfers in euros within the space. This includes banks, authorized payment entities. As already mentioned, Regulation (EU) 2024/886 sets the start of the practical application on October 9, 2025, although suppliers have additional deadlines to adapt their systems. Each Member State will supervise compliance through its national financial authority.

Images | WorldOfSoftware with Gemini 2.5 | CaixaBank

In WorldOfSoftware | In silence, a large European company has become a fundamental actor for AI: the Swiss National Bank

{kind=link}