Oracle (ORCL 3.93%) is delivering explosive growth in artificial intelligence (AI) infrastructure, with phenomenal demand for its data centers from hyperscalers and pure-play AI companies. But the market’s attention has shifted elsewhere: to the remarkable rally in DigitalOcean (DOCN 2.99%)whose shares are up 115% over the past year, compared to the modest 4% gain in Oracle stock.

Oracle’s influence in the cloud AI infrastructure market is evident in its latest quarterly results. The tech giant reported a whopping 325% year-over-year increase in remaining performance obligations (RPO) in the third quarter of fiscal 2026 (which ended February 28) to a massive $553 billion. That’s well above the $67 billion in revenue Oracle expects for the current fiscal year, suggesting the company is poised for years of excellent growth.

Still, investors have been drawn to DigitalOcean, a much smaller data center infrastructure provider.

Let’s take a look at the factors driving DigitalOcean’s remarkable rise and consider why it’s built for greater upside.

Image source: Getty Images.

DigitalOcean’s focus on small customers pays off

Oracle’s enormous revenue shortfall is caused by the large-scale contracts it has concluded with companies such as OpenAI, Metaplatforms, Microsoftand others. However, these large contracts have negatively impacted Oracle’s stock, especially its relationship with OpenAI.

Investors are concerned about whether OpenAI can raise the money needed to pay Oracle, especially as the latter has taken on huge amounts of debt to finance the expansion of its infrastructure.

DigitalOcean, on the other hand, has a different business model. The on-demand cloud computing platform is suitable for developers, small and medium businesses and start-ups. Simply put, DigitalOcean is a non-hyperscaler cloud computing provider that reduces the complexity and additional costs associated with running workloads in a hyperscaler environment.

Today’s change

(-2.99%)$-2.55

Current price

$82.80

Key data points

Market capitalization

$7.6 billion

Day range

$80.70 -$85.54

Range of 52 weeks

$25:45 -$86.50

Volume

123K

Avg. full

3.1 million

Gross margin

59.86%

In 2022, an external report from market research firm Forrester noted that DigitalOcean was 50% cheaper than hyperscalers. So, it’s easy to understand why the company has witnessed robust growth in its customer base and is building a strong future revenue pipeline.

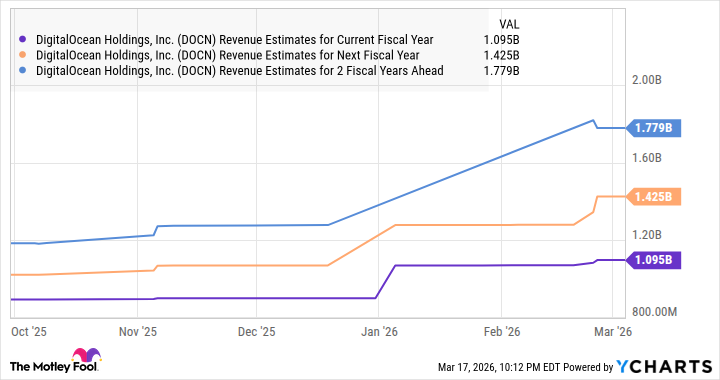

DigitalOcean’s 2025 revenue rose 15% to $901 million. The company has raised its growth estimates for 2026 and 2027, driven by strong customer growth and improved traction for its AI solutions. DigitalOcean expects a 21% increase in revenue this year, followed by a stronger increase of 30% in 2027.

AI is an important catalyst

AI in particular is now an important catalyst for DigitalOcean. The company offers a full-stack AI infrastructure platform that allows customers to not only rent graphics cards and server processors to run workloads, but also access large language models, agentic AI tools, and managed services to build and scale AI applications.

Additionally, DigitalOcean does not bind customers to long-term contracts and offers predictable, transparent pricing. As a result, the company’s annual run rate (ARR) revenues for its AI offering rose 150% year-over-year to $120 million in the fourth quarter of 2025.

It’s worth noting that 70% of AI-focused ARR in the previous quarter came from inference services and general cloud computing services. Thus, DigitalOcean’s strategy to acquire AI data center hardware is paying off as it gains additional revenue from software-focused offerings.

The strong AI-driven demand explains why DigitalOcean will add 31 megawatts (MW) of cloud computing capacity this year. The company admits that the investments will put pressure on operating results. Still, the good news is that DigitalOcean expects to maintain a straightforward free cash flow margin of 18% to 20% despite the addition of additional capacity.

The good news is that additional capacity will increase from the second quarter of the year, indicating that DigitalOcean can quickly generate returns on its data center investments.

Investors can expect more upside from this high-flying stock

DigitalOcean’s stock trades at 8.4 times sales, which is a slight premium to the US tech sector’s average sales multiple of 8. However, that slight premium is justified by DigitalOcean’s improving growth trajectory.

DOCN revenue estimates for current fiscal year data based on YCharts.

{kind=link}