It looks like Nvidia is going to jump over an already sky-high bar in 2026.

Nvidia (NVDA +0.79%) has been dominating the artificial intelligence (AI) data center market for years with its GPU chips. The AI era started with the Hopper microarchitecture, continued with Blackwell, and now looks to Rubin, Nvidia’s most ambitious chip platform yet.

The stakes may also be the highest they’ve ever been. Not only is the market beginning to question AI hyperscalers as they pour hundreds of billions of dollars into data centers, but the AI technology itself is rapidly evolving, creating a moving target for Nvidia and others.

Rubin is in full production and will ship later this year. Is now the time to buy Nvidia stock, or is the AI chip king about to lose its crown?

Image source: Nvidia.

Rubin represents a crucial upgrade amid a shift in AI technology

Nvidia specializes in GPU chips that excel in high-performance computing, such as training AI models. That’s still important as OpenAI and other AI companies develop more advanced models. But now AI is quickly shifting to inference. Deloitte Global predicted that compute for inference will overtake training this year.

Okay, what does that mean?

Think of AI chips as engines in a car. The raw power of a GPU would be great for going really fast in a straight line, like in a drag race. But inference is a different kind of computing, a different kind of race. If it were a car, the winding mountain roads would require a more refined engine. In AI, inference computation involves strong, persistent reasoning capabilities for applications such as AI agents. In these situations, efficiency and speed trump raw maximum power.

Today’s change

(0.79%)$1.49

Current price

$191.31

Key data points

Market capitalization

$4.6 tons

Day range

$189.58 -$193.95

Range of 52 weeks

$86.62 -$212.19

Volume

6.2 million

Avg. full

174M

Gross margin

70.05%

Dividend yield

0.02%

Rubin is not a single GPU; it’s six components, including CPUs and GPUs, network switches and interfaces, all working together as an AI supercomputer. Nvidia designed Rubin with inference in mind. The Vera Rubin NVL72 server rack-mounted superchip performs inference computing at 10% of the cost per million tokens compared to Nvidia’s current flagship Blackwell GB200 NVL72.

Nvidia should maintain its growth momentum

AI hyperscalers are under pressure to realize a return on their AI spend, and the dramatic improvements in inference efficiency will likely be a strong selling point for Rubin. Nvidia announced in November that it already had a $500 billion order book through 2026, and that this is likely to increase further once it reports its latest earnings results on February 25. Nearly every AI hyperscaler plans to spend even more on AI by 2026.

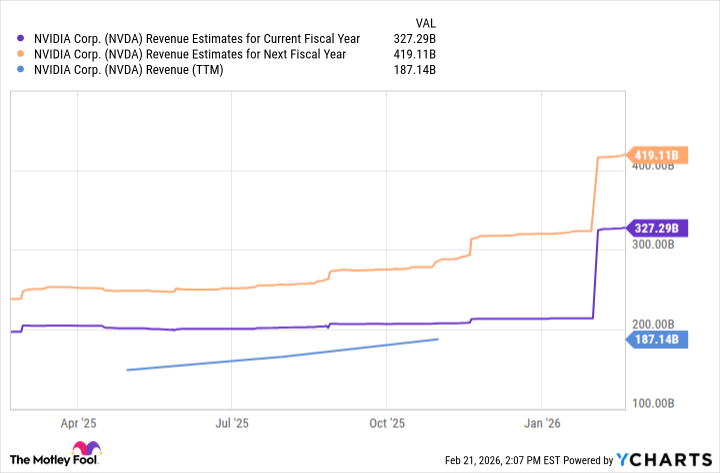

Data per YCharts.

Wall Street analysts certainly expect big things for Nvidia. Estimates expect the company’s last-12-month revenue to rise from $187 billion to about $327 billion this fiscal year, and $419 billion next year. Furthermore, Nvidia has exceeded Wall Street’s quarterly revenue expectations without fail for the past three years, so it wouldn’t be a surprise if the actual numbers were even higher.

Is this the time to buy the shares?

Nvidia shares trade at nearly 25 times sales. If the company performs as expected, the shares will become much cheaper quite quickly. The shares trade at just 11 times next year’s revenue forecast. It’s worth noting that Nvidia relies on a highly concentrated customer base, and one or more hyperscalers scaling back their AI spending could quickly turn these estimates upside down.

While Nvidia still has the lion’s share of installed AI data center chips, it must continue to fend off competition, especially as customers place more emphasis on cost savings. Broadcom has already had great success in collaboration with Alphabet on Tensor Processing Units (TPUs) for its AI models.

Nvidia will likely remain an AI winner in the long term due to its entrenched leadership and the future growth opportunities for AI as a whole. Investors may want to wait a little longer, or at least keep buying, until Nvidia updates shareholders with its latest outlook after earnings reports.

{kind=link}