Stock prices of Cirrus logic (NASDAQ: CRUS) are in good shape so far in 2024, with gains of 48% as Wall Street turns optimistic about the chipmaker’s prospects. The market is excited about a turnaround in the smartphone market, solid quarterly results and a potential improvement in the fortunes of its biggest customer – Apple (NASDAQ: AAPL).

After all, Cirrus relies heavily on Apple for a large portion of its revenue. In the recently concluded fiscal year 2024 (which ended March 30), Apple accounted for a whopping 87% of Cirrus’ revenue. Apple’s share of Cirrus’ revenue has been growing in recent years. Apple contracts accounted for 83% and 79% of revenue in the previous two fiscal years.

While it’s not good to rely on one customer for so many things, a turnaround in Apple’s fortunes regarding its artificial intelligence (AI) efforts could be a blessing in disguise for Cirrus Logic. Here’s why.

Cirrus Logic’s largest customer can help accelerate growth

Cirrus Logic is known for delivering audio codecs, camera controllers, fast-charging chips and haptic solutions to smartphone customers like Apple. The company posted $372 million in revenue in the fourth quarter of fiscal 2024, which was flat year-over-year but crushed Wall Street estimates of $317 million. The company’s non-GAAP (adjusted) earnings jumped an impressive 35% year-over-year to $1.24 per share, nearly double the consensus estimate of $0.64 per share.

Additionally, Cirrus’ forecast of $320 million in current-quarter revenue contributed to the midpoint of guidance, adding to investor optimism as it beat analysts’ estimate of $302 million. The guidance marks a slight jump in the top line from the $317 million figure in the year-ago period.

So Cirrus’ fortune is closely tied to Apple. This explains why Cirrus’ revenue growth wasn’t solid last quarter. For example, Apple’s iPhone shipments fell nearly 10% year over year in the first quarter of 2024, according to market research firm IDC. Sales of iPads and wearables also fell. As a result, Apple’s total revenue in the second quarter of fiscal 2024 (which ended March 30) fell 4% year over year.

The good news for Cirrus Logic is that Apple’s iPhone sales are expected to increase over the course of the year, thanks to the spread of AI. Market research firm Counterpoint Research estimates that the AI smartphone market could post a compound annual growth rate (CAGR) of 65% through 2027.

While Apple doesn’t have an AI-enabled phone in its portfolio yet (unlike Samsung), the company recently announced a series of AI-related features that are expected to make their way to the next iPhone, which goes on sale later this year. From allowing users to use AI to summarize text to creating original images to transcribing phone calls, Apple has unveiled multiple features that could help it jump on the AI bandwagon.

JPMorgan analyst Samik Chatterjee believes the integration of AI-specific features into the 2024 iPhone models will likely drive a solid upgrade cycle and help Apple sell more smartphones. More specifically, Chatterjee expects Apple to sell 244 million iPhone units in fiscal 2025, which would be a 10% increase over estimated shipments in the current fiscal year. Momentum is expected to continue into fiscal 2026, with estimated shipments of 268 million units.

Furthermore, since the tech giant’s Apple Intelligence platform is only compatible with the iPhone 15 Pro series and iPads and MacBooks with M1 chips, the company could be in for a robust device upgrade cycle. JPMorgan estimates that this new upgrade cycle will be similar to what Apple saw when 5G smartphones arrived, and it’s worth noting that the tech giant’s growth skyrocketed at the time.

Additionally, Apple is expected to release MacBooks with AI-enabled chips this year, which could allow the company to tap into another potentially lucrative market. All of this bodes well for Cirrus Logic and explains why analysts have become optimistic about its prospects.

An improvement in growth could lead to more equity upside potential

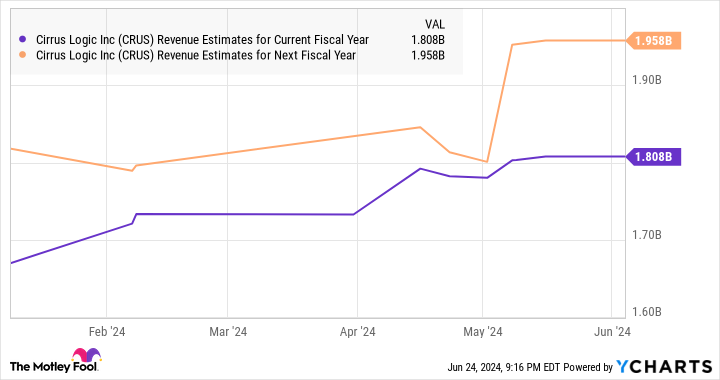

Cirrus Logic’s fiscal 2024 revenue was down nearly 6% from the previous year, to $1.79 billion. However, analysts expect the company to report a slight improvement in the current fiscal year, as shown in the following chart.

As the chart above shows, analysts have raised their revenue forecasts for the next fiscal year and expect Cirrus to deliver stronger growth. The prospects of AI-enabled smartphones and PCs and Cirrus’ relationship with a top player like Apple in these markets should help the company maintain healthy growth for a long time to come.

That’s why investors would be wise to buy Cirrus Logic stock while it’s still cheap. The semiconductor stock is currently trading at 26 times trailing earnings, a discount to the Nasdaq-100‘s trailing earnings multiple of 32 (which is used as a benchmark for technology stocks). We saw Cirrus’ earnings grow nicely last quarter, and the company was able to maintain that trend with the help of Apple.

As such, there is a good chance that Cirrus can contribute to the already impressive profits it posted in 2024.

Should You Invest $1,000 In Cirrus Logic Now?

Before you buy shares of Cirrus Logic, consider the following:

The Motley Fool stock advisor team of analysts has just identified what they think is the 10 best stocks for investors to buy now… and Cirrus Logic wasn’t one of them. The 10 stocks that made the cut could deliver monster returns in the years to come.

Think when Nvidia made this list on April 15, 2005… if you had $1,000 invested at the time of our recommendation, you would have $774,526!*

Stock Advisor offers investors an easy-to-follow blueprint for success, including portfolio building guidance, regular analyst updates, and two new stock picks each month. The Stock Advisor is on duty more than quadrupled the return of the S&P 500 since 2002*.

View the 10 stocks »

*Stock Advisor returns June 24, 2024

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool holds positions in and recommends Apple. The Motley Fool recommends Cirrus Logic. The Motley Fool has a disclosure policy.

This semiconductor stock is up 48% in 2024 and artificial intelligence (AI) could send it higher was originally published by The Motley Fool

%20Abstract%20Background%20062024%20SOURCE%20OnePlus.jpg)