stocks to buy for under in March, according to Wall Street")

SentinelOne (S 0.72%) is the cybersecurity vendor behind Singularity, an artificial intelligence (AI)-powered platform designed to automate threat detection, incident response, and everything in between. With a market capitalization of just $4.6 billion, the company is much smaller than its main rivals CrowdStrike And Palo Alto Networkswith valuations above $100 billion. But that could be an opportunity for investors.

The majority of analysts followed suit The Wall Street Journal have rated SentinelOne stock with a Buy rating, but none recommend Sell. Their consensus price target indicates strong potential upside from the current price of $13, and this is why their bullish consensus could be justified.

Image source: Getty Images.

An AI-first cybersecurity platform

Malicious actors are using technologies like AI to launch faster and more devastating cyber attacks than ever before. Human-led cybersecurity processes can no longer handle the sheer volume of breach attempts, so companies must fight fire with fire by leveraging AI-powered protection. That’s where SentinelOne’s Singularity platform comes into the picture.

Singularity is a holistic solution that protects cloud networks, employee identities, endpoints (computers and devices), and more. It includes unique features like Storyline, which reconstructs cyber attacks and produces a detailed analysis complete with recommendations, saving human cybersecurity teams hours of manual investigative work.

A powerful AI agent called Purple AI can also be embedded into Singularity for an additional fee. It is capable of making independent decisions by using advanced reasoning capabilities to identify and remediate threats in real-time. It effectively behaves like a human security analyst, but with the ability to operate at machine speed. Purple AI had a capture rate of over 50% on all licenses sold during SentinelOne’s fiscal 2026 fourth quarter (ending January 31), so it’s an extremely popular feature.

Today’s change

(-0.72%)$-0.10

Current price

$2:38 p.m

Key data points

Market capitalization

$4.9 billion

Day range

$14.24 -$14.65

Range of 52 weeks

$12.23 -$9:40 p.m

Volume

148K

Avg. full

8.4 million

Gross margin

78.74%

SentinelOne’s adjusted earnings soared in fiscal 2026

SentinelOne’s revenue grew 22% year over year to $1 billion in fiscal 2026, marking the first time the company surpassed the $1 billion milestone. Management expects revenue to grow at a more modest pace of 20% in fiscal 2027, in part because it is prioritizing profitability over outright growth.

The company’s total operating expenses rose just 13% in fiscal 2026. As revenue rose at a much faster pace, operating losses fell modestly to $321.3 million. However, after excluding one-time and non-cash expenses such as stock-based compensation, SentinelOne actually produced a non-GAAP (adjusted) gain of $68.2 million on the bottom line, a whopping 351% increase over the previous year.

That translated into adjusted earnings of $0.20 per share, which management said it could be close to double to $0.38 per share in fiscal 2027.

SentinelOne stock looks cheap compared to its rivals

The Wall Street Journal follows 39 analysts covering SentinelOne stock, and 21 have given it a buy rating. Two others are in the overweight (bullish) camp, while fifteen recommend holding. While one analyst has given the stock an underweight (bearish) rating, none recommend selling the stock.

The analysts have an average price target of $19.23, implying the stock could rise 45% over the next twelve months. The Street high target of $30 suggests there could be significantly more upside of 127% instead.

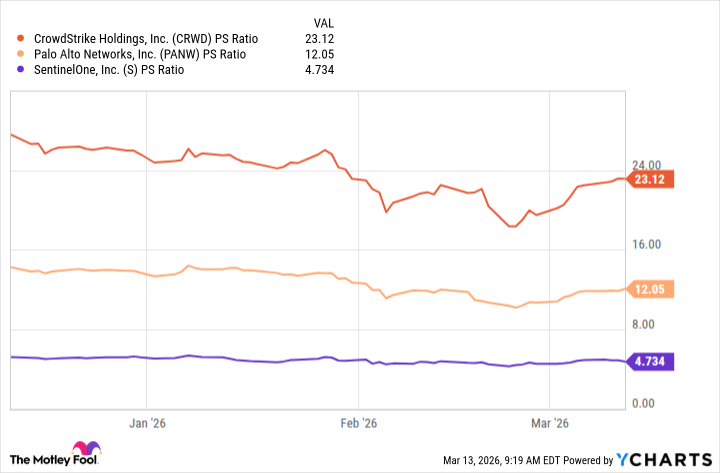

I believe these goals are achievable because of SentinelOne’s attractive valuation. It trades at a price-to-sales ratio (P/S) of just 4.7, well below its unsustainable peak of 120 in 2021, when a tech market frenzy drove its shares to irrational heights. Furthermore, it’s a steep discount to the P/S ratios of its larger rivals CrowdStrike and Palo Alto Networks:

CRWD PS Ratio data according to YCharts

CrowdStrike and Palo Alto have advantages over SentinelOne, including their incredible scale and deeper product portfolios, so they deserve their premium valuations. But even if SentinelOne stock were to rise 127% from here, its price-to-earnings ratio would only rise to 10.6, making it still cheaper than Palo Alto Networks.

Furthermore, SentinelOne values its addressable market at over $100 billion, which means it has barely scratched the surface of its capabilities based on its $1 billion in revenues in fiscal 2026. As a result, I think Wall Street is right to be bullish on this stock in the short term, but its long-term potential could be even greater.

{kind=link}