Sales and marketing software maker HubSpot (NYSE:HUBS) reported first-quarter 2024 results that beat Wall Street analyst expectations, with revenue up 23.1% year over year to $617.4 million. On the other hand, the company expects revenue to be around $618 million next quarter, slightly below analyst estimates. It posted non-GAAP earnings of $1.68 per share, an improvement from earnings of $1.20 per share in the same quarter last year.

Is Now the Time to Buy HubSpot? Find out in our full research report.

HubSpot (HUBS) Highlights Q1 CY2024:

-

Gain: $617.4 million vs. analyst estimates of $598.2 million (3.2% better)

-

EPS (non-GAAP): $1.68 vs. analyst estimates of $1.50 (12.2% better)

-

Revenue guidance for the second quarter of 2024 is $618 million in the middle, lower than analyst estimates of $623.8 million

-

Company reaffirmed its full-year revenue guidance of $2.56 billion at the center

-

Gross margin (GAAP): 84.6%, compared to 83.6% in the same quarter last year

-

Free cash flow of $99.57 million, an increase of 26.8% from the previous quarter

-

Customers: 216,840, compared to 205,091 in the previous quarter

-

Market capitalization: $31.33 billion

Founded in 2006 by two MIT students, HubSpot (NYSE:HUBS) is a software-as-a-service platform that helps small and medium-sized businesses market, sell and get found on the Internet.

Sales software

Companies must be able to communicate with their customers and sell to their customers as efficiently as possible. This reality, coupled with the continued migration of enterprises to the cloud, is driving demand for cloud-based CRM (Customer Relationship Management) software that integrates data analytics with sales and marketing functions.

Sales growth

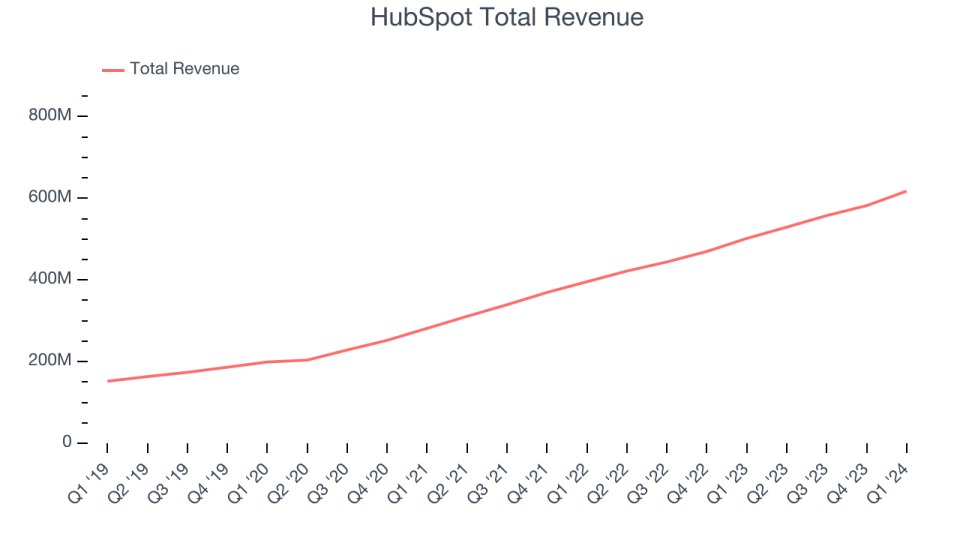

As you can see below, HubSpot’s revenue growth has been very strong over the past three years, from $281.4 million in the first quarter of 2021 to $617.4 million this quarter.

This quarter, HubSpot’s quarterly revenue rose again by a very solid 23.1% year over year. Additionally, revenue increased quarter-over-quarter by $35.5 million, a very strong improvement from the $24.36 million increase in Q4 2023. This is a sign of accelerating growth and great to see.

Guidance for next quarter shows that HubSpot expects revenue to grow 16.8% year-over-year to $618 million, a slowdown from the 25.5% year-over-year increase seen in the same quarter last year was recorded. Looking ahead, before the earnings results were announced, analysts who follow the company expected revenue to grow 17.1% over the next twelve months.

Today’s young investors probably haven’t read the timeless lessons in Gorilla Game: Picking Winners In High Technology, because it was written more than twenty years ago when Microsoft and Apple first established their supremacy. But if we apply the same principles, enterprise software stocks that leverage their own generative AI capabilities could be the gorillas of the future. In that spirit, we’re excited to present our special free report on a profitable, fast-growing business software stock that’s already riding the automation wave and looking to create the next generative AI.

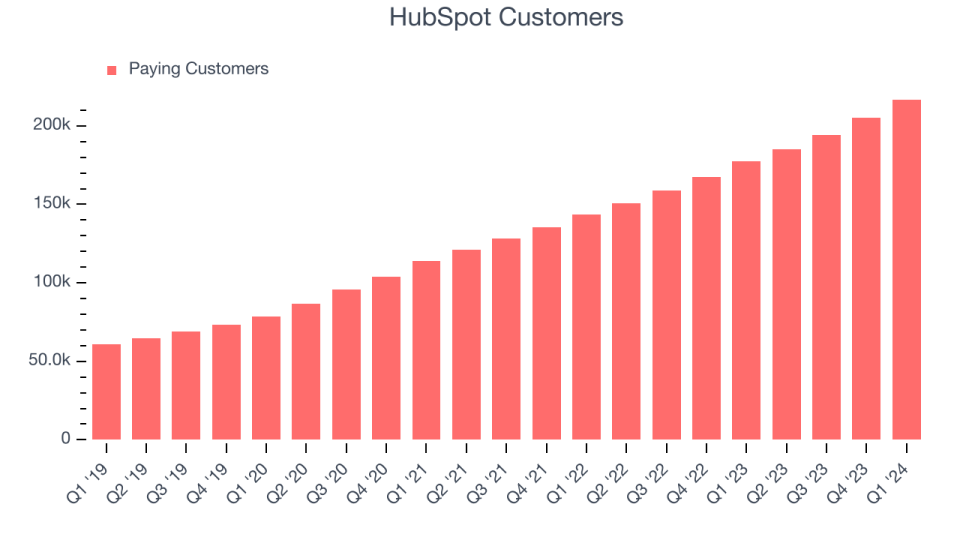

Customer growth

HubSpot reported 216,840 customers at the end of the quarter, an increase of 11,749 from the previous quarter. That’s about the same customer growth we saw last quarter and quite a bit higher than what we’ve typically seen over the past year, confirming that the company is maintaining a good sales pace.

Key takeaways from HubSpot’s first quarter results

We were pleased to see that HubSpot exceeded analyst expectations this quarter. Free cash flow was also strong, on top of an increase in sales. On the other hand, quarterly revenue expectations were slightly below Wall Street estimates, but the company seems to believe this will be made up for later in the year as full-year expectations remained unchanged. Overall, this was a decent quarter for HubSpot. The stock is up 1.9% after reporting and is currently trading at $601 per share.

So should you invest in HubSpot now? When making that decision, it is important to take into account the valuation, the business qualities and what happened in the last quarter. We cover that in our useful full research report which you can read here. It is free.