Stock Will Double in Value by the End of 2026")

Artificial intelligence (AI) stocks faced headwinds in 2026, as evidenced by the 3% decline since the beginning of the year. Global X Artificial Intelligence & Technology ETFthat invests in companies developing AI hardware and software, in addition to using the technology in their operations.

Nvidia (NVDA +2.59%)perhaps the biggest name in AI, has shared the pain of the broader market. Nvidia stock is down about 1.6% through 2026 (and was down as much as 12% at the end of March), even though there are no signs of a slowdown in business. This pullback looks like a buying opportunity, especially considering this AI pioneer could see its stock double by the end of the year.

Let’s take a look at why Nvidia could see a parabolic jump in its stock price in 2026.

Image source: Nvidia.

Nvidia’s stellar revenue pipeline will boost growth

Nvidia’s fiscal 2026 (which ended January 25, 2026) ended on a high note. Fiscal fourth quarter revenue shot up 73% year over year to $68 billion, surpassing the full year’s 65% growth to $216 billion. Earnings per share rose 82% year over year in the quarter, while annualized profits grew 60% to $4.77 per share.

The numbers are impressive, but worth noting that Nvidia will likely do even better in the new fiscal year (which coincides with most of 2026). The chipmaker’s Blackwell and Vera Rubin chip platforms have been a big hit among customers, thanks to their ability to tackle both AI model training and inference workloads.

As a result, Nvidia expects as much as $1 trillion in revenue from the Blackwell and Rubin chip systems in 2026 and 2027. That’s double the revenue it originally expected from these two platforms in 2025 and 2026, clearly suggesting that the latest Rubin systems are gaining tremendous popularity.

Today’s change

(2.59%)$4.76

Current price

$188.67

Key data points

Market capitalization

$4.6 tons

Day range

$184.32 -$190.00

Range of 52 weeks

$95.04 -$212.19

Volume

5.9 million

Avg. full

179M

Gross margin

71.07%

Dividend yield

0.02%

Again, that’s not surprising, as Nvidia claims its Rubin chips are 3.5 times faster than Blackwell during AI model training and 5 times faster for inference applications. Nvidia’s data center business therefore still has remarkable room for growth.

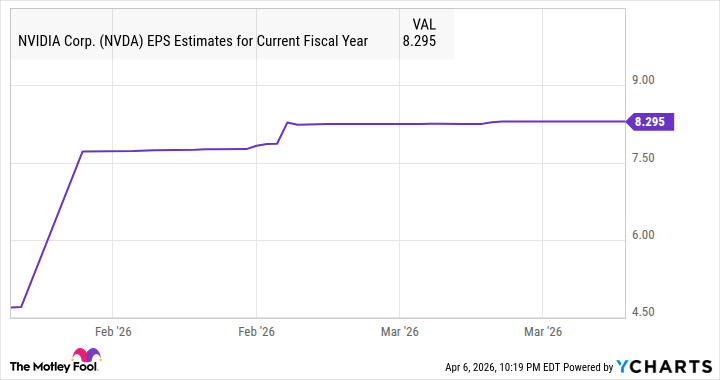

Nvidia posted a record $193.7 billion in data center revenue in fiscal 2026, up 68% from the previous year. The $1 trillion forecast over the next few years points to a substantial increase in the segment’s revenue. That’s why analysts predict a faster 74% increase in earnings to $8.29 per share this year.

Importantly, Nvidia’s FY 2027 earnings estimate came in slightly higher, a trend that could continue amid heavy investment in AI data centers.

Data per YCharts. EPS = earnings per share.

The market is not rewarding the stock for its excellent growth

The pullback of semiconductor stocks in 2026 does not seem justified given the points discussed above. As a result, Nvidia trades at an attractive 21 times forward earnings, a slight premium to the S&P500 index’s forward earnings multiple of 21. However, Nvidia deserves to trade at a much higher premium to the S&P 500.

I say this because earnings growth in the current fiscal year is expected to be more than four times the average 17% earnings growth that S&P 500 companies are expected to achieve. So don’t be surprised if this AI stock has a premium multiple after a year.

Assuming Nvidia trades at 42 times earnings due to its eye-popping growth (double the multiple of the S&P 500), the stock could jump to $348 based on estimated earnings per share of $8.29. That’s almost double the current price, which is why it would be a good idea to buy it before hitting the gas.

{kind=link}