What underlying trends should we look for in a company to find a multi-bagger stock? Ideally, a company exhibits two trends; first a growth yield on capital employed (ROCE) and secondly on an increasing quantity of the invested capital. Ultimately, this shows that it is a company that reinvests profits at increasingly higher returns. Speaking of which, we’ve noticed some big changes Beta system software (FRA:BSS) return on capital, so let’s take a look.

Return on Capital Employed (ROCE): What is it?

If you’re new to ROCE, it measures the ‘return’ (pre-tax profit) that a company generates from the capital invested in its operations. The formula for this calculation on Beta Systems Software is:

Return on Capital Employed = Earnings Before Interest and Taxes (EBIT) ÷ (Total Assets – Current Liabilities)

0.24 = €7.9 million ÷ (€64 million – €31 million) (Based on the last twelve months to September 2023).

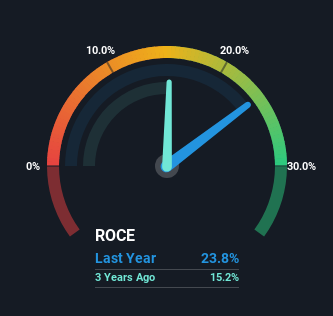

So, Beta Systems Software has a ROCE of 24%. In absolute terms, that’s a great return and it’s even better than the software industry average of 14%.

Check out our latest analysis for Beta Systems Software

In the chart above, we compared Beta Systems Software’s past ROCE to its past performance, but the future is arguably more important. If you want to see what analysts are predicting for the future, check out our free analyst report for Beta Systems Software.

What can we infer from Beta Systems Software’s ROCE trend?

Beta Systems Software has not disappointed in terms of ROCE growth. The data shows that returns on capital have increased by 172% over the past five years. The company now earns $0.2 per dollar of invested capital. In terms of capital invested, Beta Systems Software appears to be achieving more with less, as the company uses 33% less capital to run its operations. A company that shrinks its assets in this way is generally not typical of a company that will soon become a multi-bagger company.

As a side note, we noticed that the improvement in ROCE appears to be partly fueled by an increase in short-term debt. Short-term debt has risen to 48% of total assets, meaning the company is now increasingly financed by suppliers or short-term creditors, for example. Given the relatively high ratio, we would like to remind investors that having short-term debt at this level can pose certain risks at certain companies.

Our view on beta system software ROCE

In summary, it’s great to see that Beta Systems Software has managed to turn things around and achieve higher returns with lower amounts of capital. And investors seem to expect more of this in the future, as the stock has rewarded shareholders with a 90% return over the past five years. That’s why we think it’s worth checking whether these trends will continue.

One more thing to note: we’ve identified it 1 warning sign with Beta Systems Software and understanding it should be part of your investment process.

Beta Systems Software is not the only stock that generates high returns. If you want to see more, check out our free list of companies that deliver high returns on equity with solid fundamentals.

Do you have feedback on this article? Worried about the content? Please contact us directly from us. You can also email the editorial team (at) Simplywallst.com.

This article from Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts using only an unbiased methodology and our articles are not intended as financial advice. It is not a recommendation to buy or sell any stock and does not take into account your objectives or financial situation. We aim to provide you with targeted, long-term analysis based on fundamental data. Please note that our analysis may not take into account the latest price-sensitive company announcements or quality material. Simply Wall St has no positions in the stocks mentioned.